June 2026 is the first month that tests the new direct-tax machinery in real time. The first advance-tax instalment for Tax Year 2026-27 falls due on 15 June 2026 under the Income-tax Act, 2025, and the month closes three annual windows together on 30 June: Form DPT-3, the GSTR-4 composition return, and the mandatory IEC updation. Employers must also hand out Form 16 for FY 2025-26 by 15 June. This calendar maps every June due date, the law behind it, and the cost of missing it.

A recurring transition theme runs through the month. Deductions, collections and advance tax for the period from 1 April 2026 are governed by the Income-tax Act, 2025; but anything that closes out FY 2025-26, the Q4 TDS wrap-up, Form 16 and Form 16A, continues to be checked against the Income-tax Act, 1961. Per the Income Tax Department’s own transition guidance, the e-filing portal supports both Acts concurrently, and taxpayers must select the correct period when paying tax.

June 2026 at a Glance

Advance Tax Under the New Act

15 June 2026 is the first advance-tax instalment due under the Income-tax Act, 2025 for income earned in Tax Year 2026-27 (FY 2026-27).

Under Section 404 of the Income-tax Act, 2025, any taxpayer whose estimated tax liability for the year exceeds ₹10,000, after reducing expected TDS and TCS, must pay advance tax.

The instalment schedule remains unchanged: 15% by 15 June, 45% by 15 September, 75% by 15 December, and 100% by 15 March.

Top Due Dates Not To Miss

These are the highest-stakes June 2026 deadlines, ordered by risk. A delay on any of them triggers interest, a daily penalty, or – for IEC – an automatic shutdown of trade. The detailed, head-wise tables follow further down.

| No | Due Date | Compliance | Who Should Care |

|---|---|---|---|

| 1 | 15 Jun 2026 | Advance Tax: 1st instalment (15%), Tax Year 2026-27 | Every taxpayer with an estimated annual tax above ₹10,000 (business income, capital gains, rent, interest, dividends) |

| 2 | 30 Jun 2026 | Form DPT-3 – Return of Deposits (FY 2025-26) | Every non-government company with loans, advances or deposits outstanding as on 31 Mar 2026 |

| 3 | 30 Jun 2026 | GSTR-4 – Composition Annual Return (FY 2025-26) | Every composition-scheme taxpayer |

| 4 | 30 Jun 2026 | IEC Annual Updation – window closes | Every IEC holder (importers and exporters) |

| 5 | 15 Jun 2026 | Form 16 (salary) and Form 16A (Q4 non-salary) issuance | Every deductor – companies, LLPs, firms, employers |

| 6 | 07 Jun 2026 | TDS / TCS deposit for May 2026 (Challan 281) | Every non-government deductor and collector |

| 7 | 15 Jun 2026 | EPF and ESI contributions for May 2026 | Every covered employer |

| 8 | 20 Jun 2026 | GSTR-3B (Monthly) for May 2026 | Taxpayers with a turnover of over ₹ 5 crore and monthly filers |

Income Tax & TDS – June 2026

June involves a split workload: paying the first advance tax instalment for Tax Year 2026-27 under the Income-tax Act, 2025, and completing the FY 2025-26 wrap-up by issuing TDS certificates. Section 408 of the 2025 Act mandates four standard advance tax dates, while Rule 31 of the 1962 Rules still governs Form 16 and 16A issuance for the previous year. May 2026 deductions follow the 2025 Act framework.

| Due Date | Purpose | Period | Description |

|---|---|---|---|

| 07 Jun 2026 | TDS/TCS Deposit | May 2026 | Deposit TDS deducted during May 2026. These are deductions of FY 2026-27, governed by the Income-tax Act, 2025; |

| 14 Jun 2026 | TDS Certificates (Form 16B / 16C / 16D / 16E) | Apr 2026 | Certificates for tax on property purchase, rent, contractor/professional payments and virtual digital asset transactions for April 2026 deductions. |

| 15 Jun 2026 | Advance Tax – 1st Instalment (15%) | Tax Year 2026-27 | First instalment for FY 2026-27 under Section 404 read with Section 408 of the Income-tax Act, 2025. Payable where the estimated annual tax exceeds ₹10,000. |

| 15 Jun 2026 | Form 24G (Book-Adjustment Statement) | May 2026 | Government offices that paid TDS/TCS for May 2026 without a challan furnish Form 24G. |

| 15 Jun 2026 | Form 16 (Salary TDS Certificate) | FY 2025-26 | Annual salary TDS certificate for FY 2025-26, issued to every employee from TRACES. Governed by the Income-tax Act, 1961, read with Rule 31. |

| 15 Jun 2026 | Form 16A (Non-Salary TDS Certificate) – Q4 | Q4 FY 2025-26 | Non-salary TDS certificates for Q4 (Jan-Mar 2026), issued within 15 days of the 31 May Q4 return due date. |

| 30 Jun 2026 | Challan-cum-Statement (Form 26QB / 26QC / 26QD / 26QE) | May 2026 | For TDS on property purchase, rent, contractor/professional payments and virtual digital asset transactions during May 2026. |

A few points on the June income-tax obligations.

- The interest framework under the 2025 Act mirrors the old law: interest under Section 424 (corresponding to the old Section 234B) runs at 1% per month where less than 90% of the year’s tax is paid as advance tax, and interest under Section 425 (corresponding to the old Section 234C) applies to deferment of any instalment.

- Taxpayers under the presumptive scheme are an exception: under Section 408(2) of the Income-tax Act, 2025, they discharge their entire advance-tax liability in a single instalment by 15 March, so they have no obligation on 15 June. Form 16 and Form 16A must be downloaded with the official TRACES watermark; manually generated certificates are not valid for the deductee’s income-tax return.

GST Deadlines – June 2026

June 2026 involves regular monthly GST cycles and the key annual GSTR-4 closure for composition dealers. Monthly filers must submit May returns under the CGST Act, 2017, while QRMP taxpayers handle the second month of the April-June quarter via the optional IFF and mandatory PMT-06. Notably, the annual GSTR-4 due date was permanently moved to 30 June by Notification No. 12/2024-Central Tax.

| Due Date | Purpose (Form) | Period | Description |

|---|---|---|---|

| 10 Jun 2026 | GSTR-7 / GSTR-8 | May 2026 | GST TDS return by deductors and TCS return by e-commerce operators for May 2026. |

| 11 Jun 2026 | GSTR-1 (Monthly) | May 2026 | Monthly outward-supplies return for taxpayers with a turnover above ₹ 5 crore or those filing monthly. |

| 13 Jun 2026 | IFF (QRMP – Optional) | May 2026 | Second-month invoice push-out under QRMP; B2B value capped at ₹50 lakh for the month. |

| 13 Jun 2026 | GSTR-6 | May 2026 | Input Service Distributor (ISD) return for May 2026. |

| 13 Jun 2026 | GSTR-5 | May 2026 | Non-Resident Taxable Persons (NRTP) return for May 2026, due within 13 days after the month-end (Section 39(5), CGST Act). |

| 20 Jun 2026 | GSTR-3B (Monthly) | May 2026 | Monthly summary return – tax liability, ITC claim and net tax payment. |

| 20 Jun 2026 | GSTR-5A | May 2026 | OIDAR service providers’ monthly return for May 2026. |

| 25 Jun 2026 | PMT-06 (QRMP – Mandatory) | May 2026 | Second-month tax payment by QRMP taxpayers under the Fixed Sum or Self-Assessment Method. |

| 28 Jun 2026 | GSTR-11 | May 2026 | Statement of inward supplies by persons holding a Unique Identity Number (UIN) claiming refunds. |

| 30 Jun 2026 | GSTR-4 (Composition Annual Return) | FY 2025-26 | Annual return for composition taxpayers under Section 39 of the CGST Act; due date set at 30 June by Notification No. 12/2024-Central Tax. |

| As needed | RFD-11 (LUT) for FY 2026-27 | FY 2026-27 | Exporters who have not yet filed their Letter of Undertaking for FY 2026-27 should do so before making any zero-rated supply. |

A few GST watch-points for June.

- GSTR-4 and CMP-08 are not interchangeable: CMP-08 is the quarterly tax payment, while GSTR-4 is the annual reconciliation – a composition dealer must file both.

- Returns can no longer be filed more than 3 years after their due date, so older composition returns should be regularised now.

- ITC reconciliation for FY 2025-26 remains a priority: the last date to claim unclaimed input tax credit is 30 November 2026 or the GSTR-9 filing date, whichever is earlier, under Section 16(4) of the CGST Act. Composition dealers have no monthly return in June; their next CMP-08 (for Q1 FY 2026-27) falls in July.

ROC, Company & LLP – June 2026

June’s corporate calendar centres on Form DPT-3 and the ongoing CCFS 2026 window. Under Rules 16 and 16A of the Companies (Acceptance of Deposits) Rules, 2014, all non-government companies must file DPT-3 by 30 June to report deposits, loans, or other receipts as of 31 March. Additionally, the Companies Compliance Facilitation Scheme, 2026, remains open until 15 July, allowing companies to regularise overdue annual filings under Sections 460 and 403 of the Companies Act, 2013.

| Due Date | Purpose (Form) | Authority | Description |

|---|---|---|---|

| 30 Jun 2026 | DPT-3 – Return of Deposits | MCA / ROC | Annual return of deposits and non-deposit receipts (loans, advances, inter-corporate deposits) outstanding as on 31 Mar 2026, filed under Rule 16 / 16A of the Deposit Rules. Applies to all companies except government companies. Auditor-certified figures are required. See the Setindiabiz guide on DPT-3 filing. |

| Operational till 15 Jul 2026 | CCFS 2026 – Scheme Window Continues | MCA / ROC | MCA General Circular No. 01/2026 dated 24 February 2026. Companies with overdue annual returns or financial statements can file at normal fees plus only 10% of the accumulated additional fee (a 90% waiver). For the operative wording on eligible forms, fee relief and immunity, refer to the circular directly and the Setindiabiz CCFS 2026 explainer. |

Two points on the ROC items.

- First, DPT-3 catches more than formal deposits: director loans (which are exempt deposits but still reported), inter-corporate deposits, security deposits and other non-deposit receipts under Rule 2(1)(c) all go into the return; a nil position with no opening or closing balance generally need not be filed, though many companies file a nil return as a precaution. Late or non-filing attracts a fee of up to ₹5,000 on the company and every officer in default, with a continuing penalty of ₹500 per day under Rule 21, and a breach of the deposit norms themselves can attract the far heavier consequences under Section 73 of the Companies Act, 2013.

- Second, companies that left annual filings pending should use the CCFS 2026 window early in June rather than waiting for the closing weeks, when the MCA portal load typically surges; companies already struck off, under liquidation or facing IBC proceedings are not eligible.

EPF & ESI – June 2026

Provident fund and ESI obligations follow their fixed monthly rhythm in June. Employers deposit contributions for the May 2026 wage month and file the Electronic Challan cum Return. Under Section 7Q of the EPF & MP Act, 1952, a delay attracts interest at 12% per annum, and damages apply under Para 32A of the EPF Scheme and the latest EPFO notifications; ESI dues run in parallel under the ESI Act, 1948.

| Due Date | Compliance | Period | Particulars |

|---|---|---|---|

| 15 Jun 2026 | EPF and ESI Contributions | Wage Month: May 2026 | Deposit contributions and file ECR. Delays attract interest at 12% p.a. under Section 7Q of the EPF Act, plus damages under Para 32A of the EPF Scheme. |

In addition to deposits, June is ideal for finalising new-joiner tasks like UAN generation, PF KYC seeding, and ESI IP creation to prevent ECR rejections. Timely PF/ESI deposits are crucial, as late payments of employee contributions are disallowed for income-tax purposes.

DGFT & RBI – June 2026

The dominant DGFT item this month is the IEC updation deadline. Under DGFT Notification No. 58/2015-2020, every IEC holder must electronically update or confirm their IEC details on the DGFT portal between 1 April and 30 June each year – and this is mandatory even when nothing has changed. On the RBI side, the monthly ECB return continues, and FDI reporting runs on its event-based clock.

| Due Date | Purpose (Form) | Period | Description |

|---|---|---|---|

| 30 Jun 2026 | IEC Annual Updation – Window Closes | FY 2026-27 | All IEC holders complete annual verification/updation on the DGFT portal under Notification No. 58/2015-2020. Confirmation with no changes is free; modifications attract a nominal fee. Non-updation by 30 June leads to automatic deactivation of the IEC, blocking customs clearance and trade until reactivation. See Setindiabiz IEC renewal. |

| Within 7 working days from the month-end (as applicable) | RBI Form ECB-2 | May 2026 | Monthly External Commercial Borrowing return through the RBI FIRMS portal. Actual date may vary with bank holidays. |

| 15 Jul 2026 (upcoming) | FLA Return | FY 2025-26 | The annual Foreign Liabilities and Assets return to RBI under FEMA is due 15 July; companies with FDI or overseas investment should begin compiling data in June. |

| As applicable | FC-GPR / FC-TRS | As applicable | FC-GPR within 30 days of allotment of shares to foreign investors; FC-TRS within 60 days of a resident–non-resident share transfer. Both filed through the RBI FIRMS portal. |

A deactivated IEC is not permanent – it can be reactivated by completing the overdue updation – but reactivation can stall live shipments and banking, so the confirmation is worth doing well before 30 June. The updation is also an opportunity to correct the address, bank account, and contact details on the DGFT record.

Professional Tax – June 2026

Professional Tax due dates and slabs vary by state and change under the respective State Acts and Finance Acts. The table below lists indicative June due dates for high-volume employer states and is illustrative only. Always verify the current date and slab on the relevant state Professional Tax portal before filing.

| State | Indicative Due Date (Jun) | Frequency |

|---|---|---|

| Andhra Pradesh | 10 Jun | Monthly |

| Telangana | 10 Jun | Monthly |

| Karnataka | 20 Jun | Monthly |

| West Bengal | 21 Jun | Monthly |

| Maharashtra | 30 Jun | Monthly |

For the full multi-state monthly schedule and state-wise PT slabs, refer to the state-wise Professional Tax guide on setindiabiz.com.

|

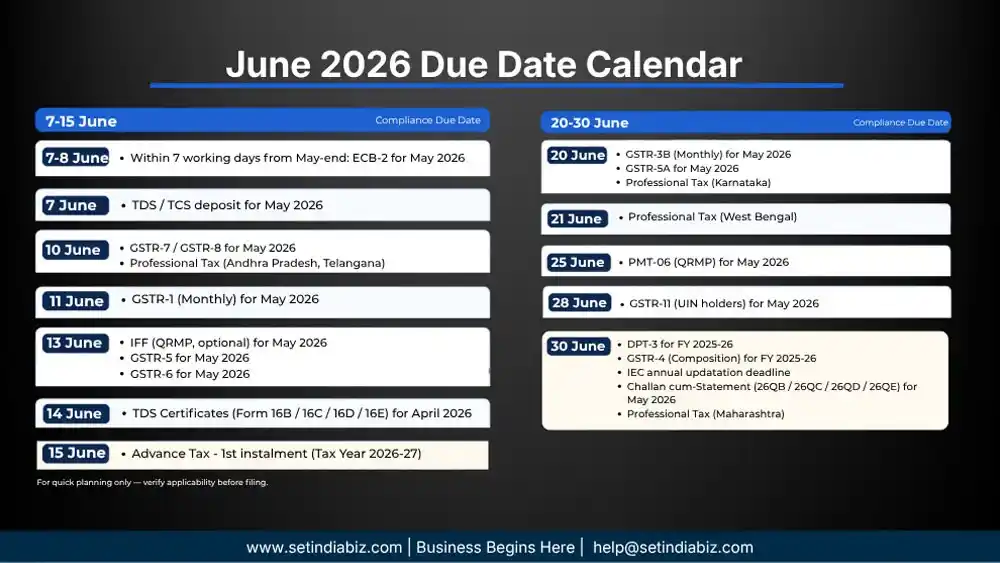

June 2026 at a Glance

A consolidated, date-ordered view of the month’s deadlines for quick planning |

|

|---|---|

| Date | Compliance |

| 7-8 June | Within 7 working days from May-end: ECB-2 for May 2026 |

| 7 June | TDS / TCS deposit for May 2026 |

| 10 June |

|

| 11 June | GSTR-1 (Monthly) for May 2026 |

| 13 June |

|

| 14 June | TDS Certificates (Form 16B / 16C / 16D / 16E) for April 2026 |

| 15 June |

|

| 20 June |

|

| 21 June | Professional Tax (West Bengal) |

| 25 June | PMT-06 (QRMP) for May 2026 |

| 28 June | GSTR-11 (UIN holders) for May 2026 |

| 30 June |

|

Penalty Matrix – Quick Reference

The figures below are illustrative, based on current provisions. Compute actual liability on the respective portal or per the latest notification before paying.

| Compliance | Penalty Structure | Additional Consequences |

|---|---|---|

| Advance Tax – 1st instalment | Interest under Section 425 of the Income-tax Act, 2025 (1% or 3% per month, corresponding to the old Section 234C) for deferment of the instalment; interest under Section 424 (1% per month, corresponding to the old Section 234B) if less than 90% of the year’s tax is paid as advance tax | Higher year-end interest cost; cash-flow drag |

| TDS Deposit – May 2026 | Interest at 1.5% per month from the date of deduction to the date of deposit for late deposit. [VERIFY: confirm the Income-tax Act, 2025 section that now replaces Section 201(1A) of the 1961 Act.] | Prosecution risk for deliberate non-deposit |

| GSTR-1 / GSTR-3B (Monthly) | Late fee of ₹50 per day (₹20 per day for nil returns) under Section 47 of the CGST Act, subject to turnover-based caps; interest at 18% p.a. on unpaid tax | Buyer’s ITC delayed; e-way bill generation may be blocked after consecutive defaults |

| GSTR-4 (Composition Annual) | Late fee of ₹50 per day (₹20 per day for nil), capped at ₹2,000; cannot be filed beyond three years from the due date | Composition-scheme eligibility at risk of persistent default |

| DPT-3 | Up to ₹5,000 on the company and every officer in default, with a continuing penalty of ₹500 per day under Rule 21 of the Deposit Rules | Breach of deposit norms attracts consequences under Section 73 of the Companies Act, 2013; ROC scrutiny |

| EPF / ESI | Interest at 12% p.a. under Section 7Q of the EPF Act, plus damages under Para 32A of the EPF Scheme | Disallowance of late-deposited employees’ contribution under the income-tax law |

| IEC Updation (if missed by 30 Jun) | No late fee, but the IEC is automatically deactivated after 30 June 2026 | Customs clearance, trade banking and export incentives are blocked until the IEC is reactivated |

Frequently Asked Questions

Why is the first advance-tax instalment due on 15 June 2026, and is it under the new Act?

Advance tax for FY 2026-27 is governed by the Income-tax Act, 2025. Under Section 404, taxpayers with an estimated liability exceeding ₹10,000 must pay in four instalments (15%, 45%, 75%, and 100%), starting 15 June. While the schedule remains unchanged from the previous law, Section 408(2) exempts presumptive scheme taxpayers from the June deadline as they pay in a single instalment by 15 March.

Who must file Form DPT-3 by 30 June 2026, and what does it cover?

Every company except a government company must file Form DPT-3 under Rule 16 (and the one-time return under Rule 16A) of the Companies (Acceptance of Deposits) Rules, 2014. The annual return reports both deposits accepted under Chapter V of the Companies Act, 2013, and money received that is not treated as a deposit—such as director loans, inter-corporate deposits, security deposits and other receipts under Rule 2(1)(c)—outstanding as on 31 March 2026. The figures must be certified by the company’s auditor. The due date is 30 June 2026 for FY 2025-26, and late filing attracts a fee of up to ₹5,000 plus ₹500 per day of continuing default under Rule 21.

Is GSTR-4 for FY 2025-26 due in June 2026?

Yes. The GSTR-4 annual return for composition taxpayers for FY 2025-26 is due by 30 June 2026. The due date was permanently shifted from 30 April to 30 June for FY 2024-25 onwards, following the 53rd GST Council meeting and Notification No. 12/2024-Central Tax dated 10 July 2024. GSTR-4 is separate from CMP-08. CMP-08 is the quarterly self-assessed tax payment, while GSTR-4 is the once-a-year consolidation, and a composition dealer must complete both. A GSTR-4 cannot be filed beyond three years from its due date, so any older composition returns should be regularised promptly.

What happens if I miss the IEC updation deadline on 30 June 2026?

Under DGFT Notification No. 58/2015-2020, every IEC holder must update or confirm their IEC details on the DGFT portal between 1 April and 30 June each year, even if nothing has changed. If you miss 30 June 2026, your IEC is automatically deactivated, which blocks customs clearance, freezes international trade banking and stalls export-incentive applications until the code is reactivated. Confirmation with no changes is free of cost, while modifications attract a nominal fee. A deactivated IEC can be reactivated by completing the overdue updation, but the disruption to live shipments usually costs far more than the update itself.

When must Form 16 and Form 16A be issued for FY 2025-26?

After the Q4 TDS return was filed by 31 May 2026, Form 16 (the annual salary TDS certificate) must generally be issued to every employee by 15 June 2026 for FY 2025-26. Form 16A for non-salary TDS for Q4 must also be issued within 15 days of the Q4 return due date—effectively 15 June 2026. Both are governed by the Income-tax Act, 1961, read with Rule 31 of the Income-tax Rules, 1962, because they relate to FY 2025-26. Both certificates must be downloaded from the TRACES portal with the official watermark; certificates without the watermark are not valid for the employee’s or vendor’s income-tax return.

Do QRMP taxpayers have any June 2026 GST obligations?

Yes, two. June is the second month of the April–June quarter for QRMP taxpayers. The Invoice Furnishing Facility (IFF) for May 2026 invoices is optional and due by 13 June. It is useful for large B2B suppliers who want their customers’ input tax credit to flow without waiting for the quarterly GSTR-1 in July. The PMT-06 tax payment for May 2026, however, is mandatory for all QRMP taxpayers and is due by 25 June, payable under the Fixed Sum or Self-Assessment Method. The quarterly GSTR-1 and GSTR-3B for the April–June quarter fall due in July, not June.

Which law governs my June 2026 TDS and advance tax — the 1961 Act or the 2025 Act?

It depends on the period the obligation belongs to. Deductions, collections and advance tax for income from 1 April 2026 onwards are governed by the Income-tax Act, 2025. Therefore, your May 2026 TDS deposit (7 June) and your first advance-tax instalment for Tax Year 2026-27 (15 June) follow the new Act. Anything that closes out FY 2025-26 continues under the Income-tax Act, 1961. Hence, the Form 16 and Form 16A issued by 15 June, and the Q4 reconciliation behind them, are checked against the old Act. The Income Tax Department’s e-filing portal supports both Acts together; select the correct period when making payments.

Where should businesses verify June 2026 due dates officially?

For income-tax dates, refer to the Income Tax Department tax calendar and the e-filing portal at incometax.gov.in. For GST, refer to gst.gov.in and the latest CBIC notifications. For ROC filings and CCFS 2026, refer to the MCA portal at mca.gov.in and MCA General Circular No. 01/2026 dated 24 February 2026. For DGFT and IEC updation, refer to the DGFT portal at dgft.gov.in and Notification No. 58/2015-2020. For EPF and ESI, refer to epfindia.gov.in and esic.gov.in.

Disclaimer: This guidance reflects laws as of Jun 1, 2026, including the Income-tax Act, 2025, Income-tax Act, 1961, Companies Act, 2013, CCFS 2026, CGST Act, 2017 (GSTR-4), EPF & MP Act, 1952, ESI Act, 1948, and DGFT IEC notifications. State-specific Professional Tax dates vary. As regulations change, verify deadlines on official portals like incometax.gov.in, gst.gov.in, mca.gov.in, dgft.gov.in, epfindia.gov.in, and esic.gov.in. This is not legal or tax advice; consult a professional for your specific needs. Setindiabiz provides comprehensive compliance support for TDS, advance tax, DPT-3, GST, and IEC to support your business growth.

In This Article

Author Bio

Setindiabiz Editorial Team is a multidisciplinary collective of Chartered Accountants, Company Secretaries, and Advocates offering authoritative insights on India’s regulatory and business landscape. With decades of experience in compliance, taxation, and advisory, they empower entrepreneurs and enterprises to make informed decisions.