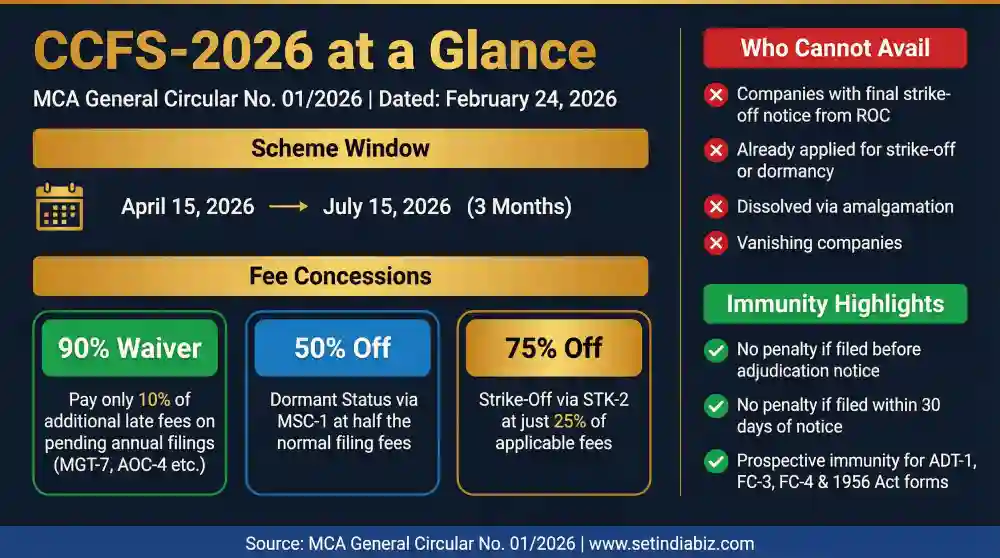

The Ministry of Corporate Affairs (MCA) introduced the Companies Compliance Facilitation Scheme, 2026 (CCFS-2026) through General Circular No. 01/2026 dated February 24, 2026. This one-time compliance window is designed to help defaulting Indian companies regularise their pending statutory filings with the Registrar of Companies (ROC). Active strictly from April 15, 2026, to July 15, 2026, the scheme allows companies to file their overdue annual returns and financial statements by paying just 10% of the accumulated additional late fees. The CCFS-2026 also offers heavily discounted legal pathways for inactive entities to either declare themselves dormant or officially strike their names from the MCA corporate registry. This initiative directly promotes ease of doing business and helps clean up the national database of companies.

What is the Companies Compliance Facilitation Scheme 2026?

The Companies Compliance Facilitation Scheme, 2026, is a temporary relief program launched by the Central Government to condone massive delays in corporate filings and reduce the financial burden on non-compliant businesses. With the number of active companies in India now crossing the 20 lakh mark, this initiative directly addresses the struggles of MSMEs, startups, One Person Companies (OPCs), and producer companies that have accumulated heavy daily penalties for failing to submit their annual statutory documents on time. By participating in this scheme during its three-month operational window, company owners can restore their active compliance status, legally pause their operations by obtaining dormant status, or close down entirely at a fraction of the standard administrative costs.

The legal authority for this scheme comes from Section 460 read with Section 403 of the Companies Act, 2013. Section 460 empowers the Central Government to condone delays in the filing of documents with the Registrar, while Section 403 governs the fees for filing documents, returns, and statements. Using this combined power, the MCA has overridden the standard late fee structure that normally imposes an additional fee of ₹100 per day for delayed annual filings — a penalty that carries no upper limit under the Companies (Registration Offices and Fees) Rules, 2014. This targeted intervention ensures that the corporate registry reflects accurate, up-to-date information while rescuing genuine entrepreneurs from crippling penalty accumulations.

What are the Fee Concessions Under CCFS-2026? 📉

The CCFS-2026 provides three distinct financial benefits depending on whether a company wants to clear its filing backlogs, temporarily pause its business operations, or shut down permanently. Each concession is specifically designed to encourage immediate legal compliance by drastically reducing the standard government filing fees. The following table provides a clear comparison of the fee structure under the scheme:

| Action | E-Form | Normal Cost | Cost Under CCFS-2026 |

|---|---|---|---|

| Clear pending annual filings | Relevant e-forms as defined under the scheme (MGT-7, AOC-4, ADT-1, FC-3, FC-4, etc.) | Normal fees + ₹100/day additional fees (no cap) | Normal fees + only 10% of additional fees |

| Apply for Dormant Status | MSC-1 (under Section 455) | Full normal filing fees | 50% of normal filing fees |

| Apply for Company Strike-Off | STK-2 (under Section 248) | Full filing fees under relevant rules | 25% of applicable filing fees |

How Much is the Waiver on Pending Annual Filings?

Active companies with a backlog of statutory filings can submit their relevant e-forms by paying the standard normal fees, along with only 10% of the total additional fees that have accrued over the delay period. Under the normal provisions of the Companies (Registration Offices and Fees) Rules, 2014, a steep additional fee of ₹100 per day is charged for late filings of annual returns (Form MGT-7/MGT-7A) and financial statements (Form AOC-4 and its variants). This daily penalty has no upper cap, meaning a company that missed filings for even three years could face additional fees running into lakhs of rupees. By waiving an unprecedented 90% of these late fees, the CCFS-2026 offers immense financial relief to startups and MSMEs attempting to regularise their historical corporate defaults.

What is the Cost to Obtain Dormant Status?

Under Section 455 of the Companies Act, 2013, an inactive company can legally apply to be declared a “dormant company” to maintain its corporate existence on the register with minimal compliance requirements. Through the CCFS-2026, companies filing e-form MSC-1 to obtain dormant status are required to pay only one-half (50%) of the normal filing fees prescribed under the rules. This is a highly cost-effective strategy for entrepreneurs who wish to shelve a business entity temporarily without incurring standard annual maintenance costs or heavy penalty accumulations. Dormant status allows a company to remain registered while significantly reducing its compliance burden.

What are the Discounted Fees for Company Strike-Off?

Governed by Section 248 of the Companies Act, 2013, the process of striking off a company’s name from the register normally requires a standard filing fee. Under the CCFS-2026, defunct companies filing e-form STK-2 for official closure are required to pay only 25% of the standard applicable filing fees mandated under the Companies (Removal of Name of Companies from the Register of Companies) Rules, 2016. This heavily discounted exit route helps entrepreneurs officially close failed ventures smoothly without incurring prohibitive closure costs.

Which E-Forms are Covered Under CCFS-2026? 📋

The circular defines “relevant e-forms” broadly, covering filing requirements under both the current Companies Act, 2013 and the erstwhile Companies Act, 1956. This means even very old pending filings dating back to the 1956 Act regime can be regularized under this scheme. The following table lists all the covered e-forms:

| Under Companies Act, 2013 | Under Companies Act, 1956 |

|---|---|

| MGT-7 (Annual Return) | Form 20B (Annual Return) |

| MGT-7A (Annual Return for OPC/Small Co.) | Form 21A (Application for Striking Off) |

| AOC-4 (Financial Statements) | Form 23AC (Balance Sheet) |

| AOC-4 CFS (Consolidated Financial Statements) | Form 23ACA (Profit & Loss Account) |

| AOC-4 NBFC (Ind AS) | Form 23AC-XBRL |

| AOC-4 CFS NBFC (Ind AS) | Form 23ACA-XBRL |

| AOC-4 (XBRL) | Form 66 (Compliance Certificate) |

| ADT-1 (Auditor Appointment) | Form 23B (Auditor Appointment Info) |

| FC-3 (Annual Return of Foreign Company) | — |

| FC-4 (Financial Statement of Foreign Company) | — |

Who is Not Eligible to Participate in CCFS-2026?

While the scheme is exceptionally broad in its coverage, it is not a blanket amnesty for all corporate entities. The MCA has explicitly defined specific categories of companies that are restricted from availing these waivers. If your company falls into one of these excluded categories, you must follow the standard legal procedures and bear the full associated costs without any concessions from the government. The following companies are not eligible to participate under CCFS-2026:

| Sr. | Category of Excluded Companies |

|---|---|

| 1 | Companies against which the Registrar has already initiated the action of final notice for striking off the name under Section 248 of the Companies Act, 2013 (previously Section 560 of Companies Act, 1956). |

| 2 | Companies which have already filed an application for striking off their name from the register of companies. |

| 3 | Companies which have already filed for obtaining dormant status under Section 455 of the Act before the inception of this scheme. |

| 4 | Companies which have been dissolved pursuant to a scheme of amalgamation under the Act. |

| 5 | Vanishing companies. |

It is important to note that the exclusion for strike-off applies specifically where the Registrar has initiated final notice proceedings suo motu under Section 248. Companies that are otherwise active but simply in default of annual filings are fully eligible to participate in the scheme and clear their backlogs at the reduced fee.

How Does the Scheme Provide Immunity from Penalties? ✅

Filing your documents under CCFS-2026 does not just save you money on filing fees. It also legally shields your company and its directors from subsequent penal actions and prosecutions related to those specific delayed filings. This legal immunity is a crucial benefit for company directors who are actively facing potential regulatory crackdowns and heavy financial penalties from the government. The immunity provisions work differently depending on the type of e-form filed.

Immunity for Annual Return & Financial Statement Defaults (Sections 92 & 137)

In accordance with the proviso to Section 454(3) of the Companies Act, 2013 (inserted by the Companies (Amendment) Act, 2020, effective January 22, 2021), proceedings regarding defaults under Section 92 (Annual Return) and Section 137 (Financial Statements) will be formally concluded without any penalty if the filings are made under the scheme in either of these two situations:

| Condition | Result |

|---|---|

| Filing made before the adjudicating officer issues a notice | Proceedings concluded — No penalty leviable |

| Filing made within 30 days of issuance of notice by the adjudicating officer | Proceedings concluded — No penalty leviable |

| Filing made after the 30-day window from notice has expired | Penalty liability remains unchanged — No relief on penalties already imposed |

| Adjudication order imposing penalty already passed | Penalty liability remains unchanged — Only filing fee benefit (10% additional fee) applies |

This is a critical distinction. The scheme provides a reduced fee for the actual filing under Section 403, but it does not reduce or waive penalties that have already been adjudicated and ordered by the adjudicating officer. The immunity from penalties is strictly available only in cases where the filings are made before or within 30 days of the issuance of a penalty notice.

Immunity for Other E-Forms (ADT-1, FC-3, FC-4 & Companies Act, 1956 Forms)

For e-forms such as ADT-1 (Auditor Appointment), FC-3 (Foreign Company Annual Return), FC-4 (Foreign Company Financial Statements), and all the legacy forms under the Companies Act, 1956 — including Form 20B, Form 21A, Form 23AC, Form 23ACA, Form 23AC-XBRL, Form 23ACA-XBRL, Form 66, and Form 23B — the immunity against prospective penal action is granted only if both of the following conditions are met:

| Sr. | Condition for Immunity |

|---|---|

| 1 | The said forms are filed under the CCFS-2026 scheme during the operational window (April 15 to July 15, 2026). |

| 2 | No prosecution has been filed, or adjudication proceedings have been initiated by issuance of a show cause notice, for such default before the filing of such forms under the scheme. |

In simple terms, if the government has already started legal proceedings against your company for not filing these specific forms, you cannot claim immunity simply by filing them under CCFS-2026. The immunity is strictly prospective and protects you only from future penal action that has not yet been initiated.

CCFS-2026 vs CFSS-2020: How Does the New Scheme Compare? 🔍

The MCA previously launched the Companies Fresh Start Scheme, 2020 (CFSS-2020) during the COVID-19 pandemic via General Circular No. 12/2020 dated March 30, 2020. While both schemes share the goal of encouraging delayed corporate filings, there are important differences in their scope, fee structure, and immunity provisions. Here is a direct comparison to help you understand what has changed:

| Parameter | CFSS-2020 | CCFS-2026 |

|---|---|---|

| Circular Reference | General Circular No. 12/2020 (March 30, 2020) | General Circular No. 01/2026 (February 24, 2026) |

| Validity Period | April 1, 2020 to December 31, 2020 (extended) | April 15, 2026 to July 15, 2026 (3 months) |

| Additional Fee Waiver | 100% waiver — Only normal fees payable | 90% waiver — Normal fees + 10% additional fees payable |

| Scope of Forms | 76 forms (much broader, including forms like DIR-12, DPT-3, MGT-14, INC-22) | Limited to annual filing forms (MGT-7, AOC-4, ADT-1, FC forms) + 1956 Act forms |

| Dormant Status Fee | Normal fees (no specific discount mentioned) | 50% of normal filing fees |

| Strike-Off Fee | Normal fees (no specific discount mentioned) | 25% of applicable filing fees |

| Immunity Certificate | Required filing of e-form CFSS-2020 separately within 6 months of scheme closure | No separate immunity form — immunity is automatic based on filing conditions under Section 454(3) proviso |

| Post-Scheme Action | ROC to take action against defaulters | ROC to take necessary action under the Act against non-availing companies |

How to Avail the CCFS-2026 Scheme: Step-by-Step Process

Availing the benefits of the CCFS-2026 scheme requires a systematic approach. While the MCA has not prescribed a separate application form for registering under the scheme (unlike CFSS-2020), companies must ensure they complete their filings on the MCA-21 portal within the scheme window with the correct fee payment. Here is a practical step-by-step guide:

| Step | Action | Details |

|---|---|---|

| 1 | Conduct a Filing Audit | Identify all pending annual returns (MGT-7/MGT-7A) and financial statements (AOC-4 and variants) for every financial year. Check for any pending ADT-1, FC-3, or FC-4 filings as well. |

| 2 | Check Eligibility | Confirm that your company does not fall in the excluded categories — no final strike-off notice from ROC, no prior application for strike-off or dormancy, not a vanishing company, and not dissolved via amalgamation. |

| 3 | Prepare Documents | Ensure all financial statements are prepared, audited (where applicable), and the annual returns are drafted. Board resolutions authorizing the filings may be required. |

| 4 | File on MCA-21 Portal | Upload and submit all relevant e-forms on the MCA-21 V3 portal between April 15, 2026, and July 15, 2026. Pay the normal fees + 10% additional fees at the time of filing. |

| 5 | Decide Your Path | Choose whether to: (a) Clear backlogs and continue as an active company, (b) File MSC-1 for dormant status at 50% fees, or (c) File STK-2 for strike-off at 25% fees. |

| 6 | Verify Payment & SRN | After successful filing, verify your Service Request Number (SRN) on the MCA portal. Retain payment receipts and challan copies for your records. |

What Happens if You Do Not Avail the CCFS-2026 Scheme?

The General Circular No. 01/2026 explicitly states that at the conclusion of the scheme on July 15, 2026, the Registrars of Companies concerned shall take necessary action under the Act against all companies that have not availed of this scheme and remain in default of filing their documents in a timely manner. In practice, this means the ROC may initiate the following enforcement actions against non-compliant companies and their officers:

The ROC can issue adjudication notices under Section 454 of the Companies Act, 2013, imposing monetary penalties on the company and every officer in default. Under the post-2020 amendment text of Section 92(5), the company and each officer in default are liable to a penalty of ₹10,000 plus ₹100 per day of continuing default, subject to a maximum of ₹2,00,000 for the company and ₹50,000 for each officer. Similarly, under the amended Section 137(3), the company is liable to a penalty of ₹10,000 plus ₹100 per day of continuing default (maximum ₹2,00,000), while the managing director, CFO, or responsible director faces a penalty of ₹10,000 plus ₹100 per day (maximum ₹50,000 each). Additionally, the Registrar may initiate suo motu strike-off proceedings under Section 248, and directors of defaulting companies may face disqualification under Section 164(2)(a) for not filing annual returns or financial statements for a continuous period of three financial years. 🚨

Conclusion

The Companies Compliance Facilitation Scheme 2026 (CCFS-2026) is a significant lifeline for Indian businesses struggling with the heavy financial burden of delayed compliance. By offering a 90% waiver on additional filing fees, a 50% discount on dormant status applications, and a 75% fee reduction for striking off defunct companies, the MCA has provided a highly practical path to legal compliance. This scheme is especially relevant for MSMEs, startups, OPCs, and private companies that have been unable to keep up with the annual filing requirements due to financial constraints or operational difficulties. Company directors and professionals must act swiftly between April 15, 2026, and July 15, 2026, to audit their pending filings and take full advantage of this scheme. Failing to do so will inevitably result in rigorous penal action by the Registrars of Companies once the amnesty window officially closes. Given that no separate application form like CFSS-2020 is required, the process is straightforward — simply complete your filings on the MCA-21 portal with the reduced fees during the scheme period.

FAQ’s

What is the duration of the Companies Compliance Facilitation Scheme 2026?

How much additional fee do I have to pay for delayed annual returns under CCFS-2026?

Can I close my inactive company using the CCFS-2026 scheme?

Does the scheme waive penalties that have already been adjudicated?

Can companies that have already applied for strike-off claim a refund under this scheme?

Is there a separate application form to register under CCFS-2026 like CFSS-2020?

What happens to companies that do not avail the CCFS-2026 scheme?

In This Article

Author Bio

Meet Sanjeev Kumar, a distinguished advocate before the Supreme Court of India, High Courts, and National Tribunals. Founding Partner of Juriskps Law Offices, a premier law firm, he specializes in commercial, corporate, tax, arbitration, and IPR matters. His incisive legal insights enrich Setindiabiz’s blog with expert commentary.