Business Structure in India: Choose the Right One

Proprietorship, partnership, LLP, OPC, private company, or public company, each decides your liability, tax, control, and compliance for years. This guide compares them side by side, and Setindiabiz process experts help you pick the right fit before you file.

🗹 Key Information of Start Your Business |

||

|---|---|---|

| 1 | What it decides | Liability, ownership, taxation, funding readiness, and annual compliance load. |

| 2 | Options covered | Sole proprietorship, partnership firm, LLP, OPC, private company, public company. |

| 3 | Governing laws | Indian Partnership Act, 1932; LLP Act, 2008; Companies Act, 2013; Income-tax Act, 2025. |

| 4 | Limited liability | LLPs, OPCs, private and public companies separate personal assets from business debts; proprietorships and partnerships do not. |

| 5 | Best for funding | Private limited companies support equity, share classes, and ESOPs (Section 2(68) of the Companies Act, 2013). |

| 6 | Lowest compliance | Sole proprietorship: no MCA filing or statutory audit, only tax and local registrations. |

| 7 | Taxation | Firms/LLPs at 30% + surcharge + cess; companies at 30% / 25% / 22% under the Income-tax Act, 2025. |

| 8 | Setindiabiz role | Compare options for your profile, then file the chosen route (SPICe+ / FiLLiP/partnership deed). |

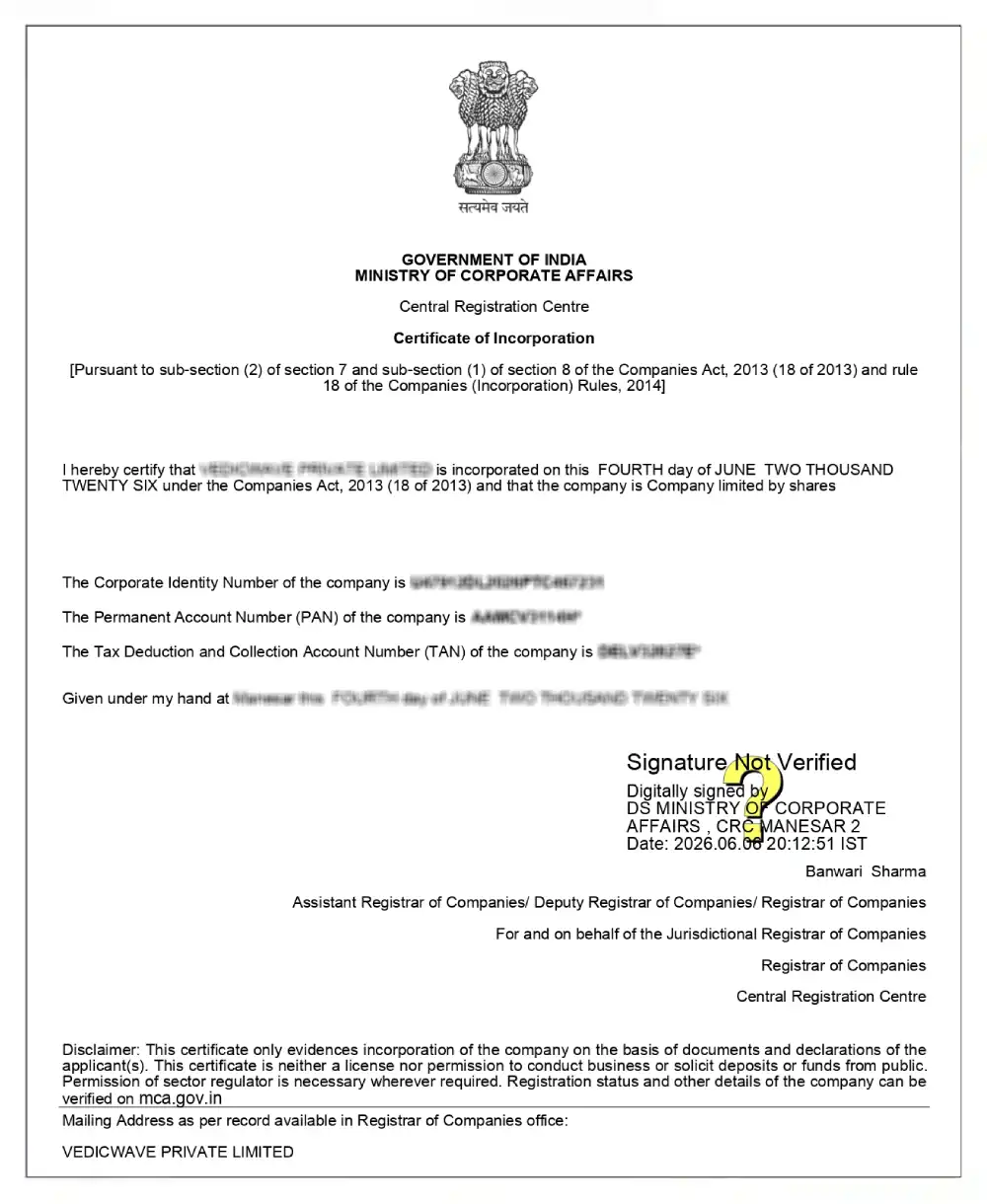

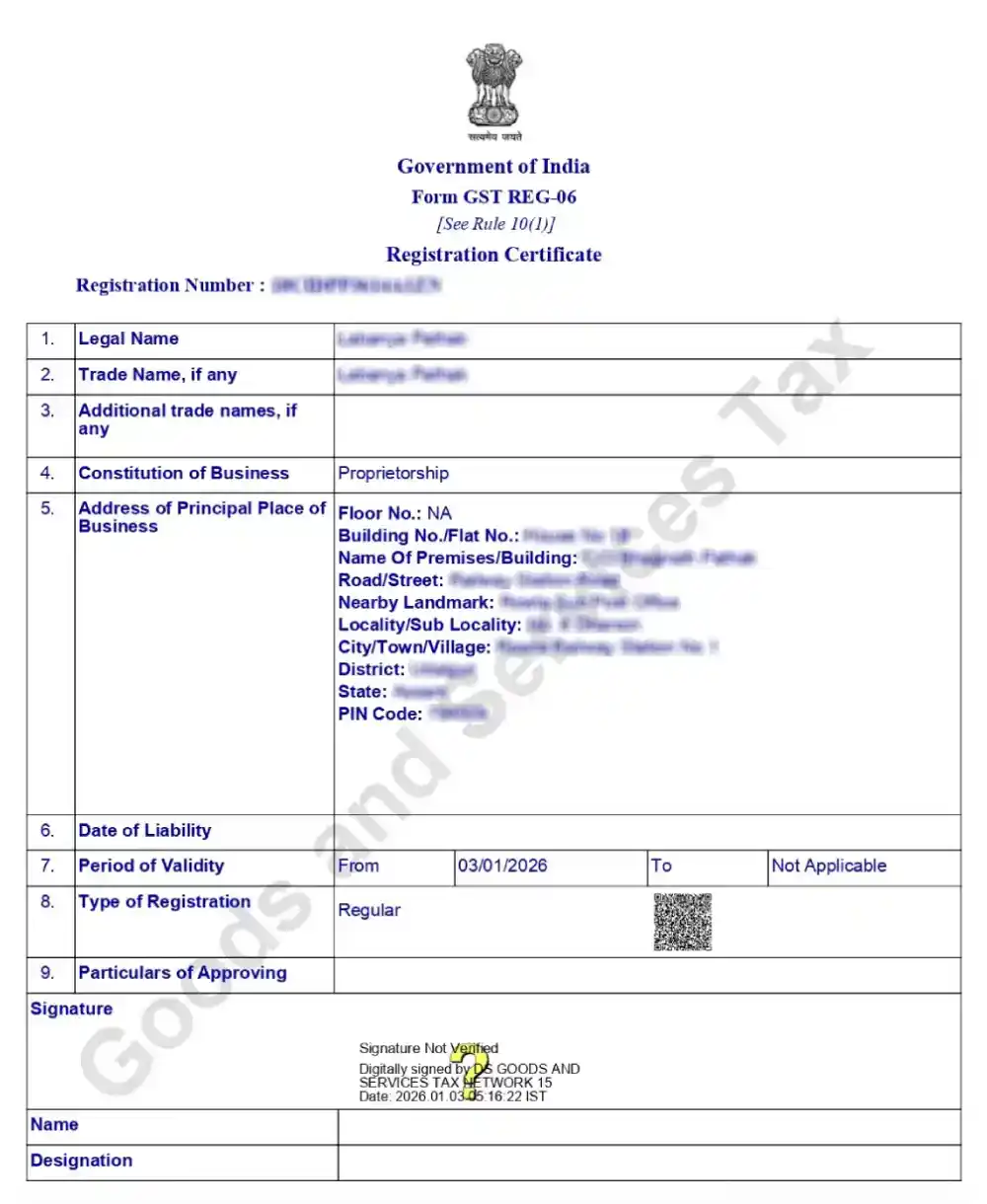

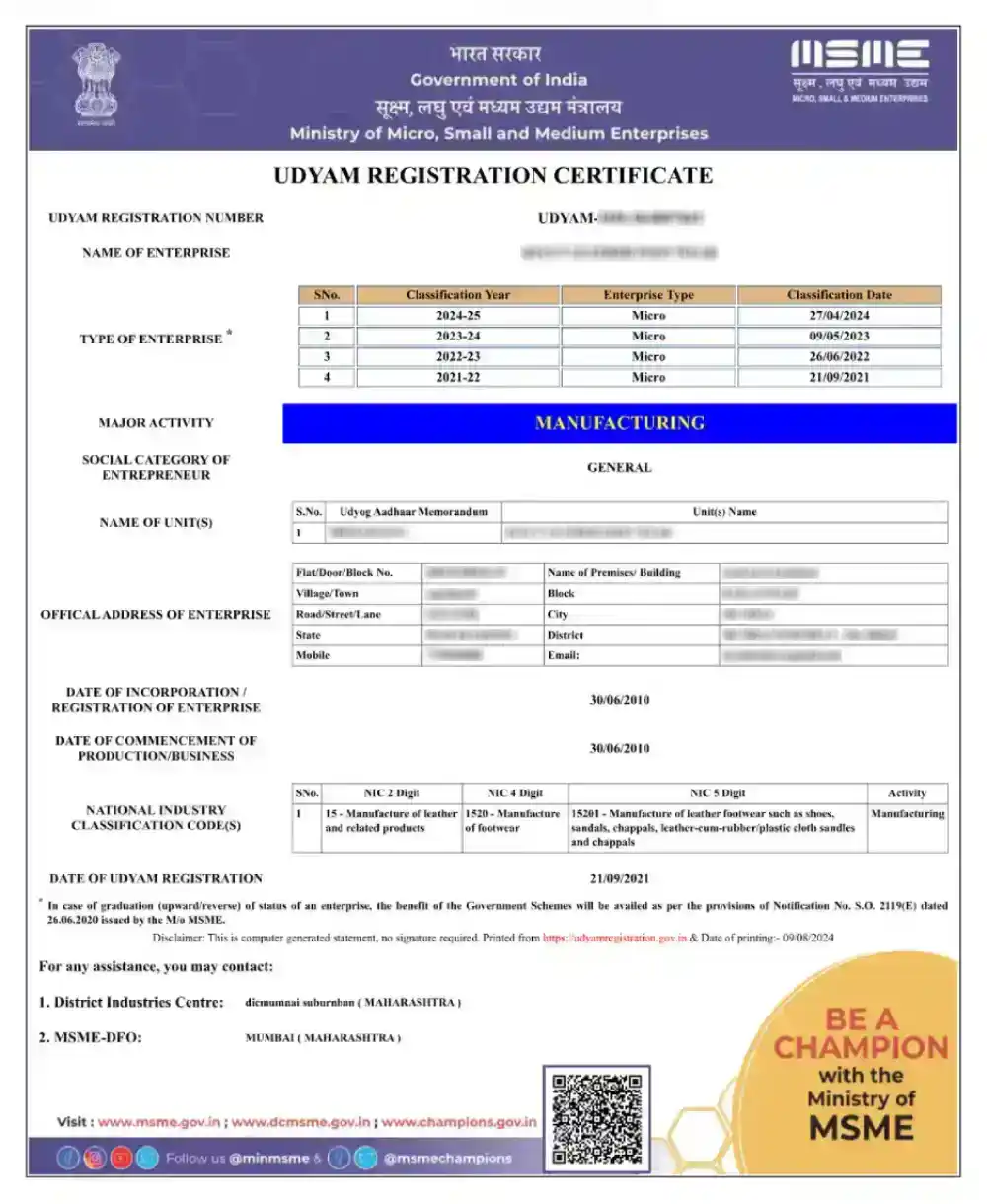

COI, GST, MSME, Trademark

What is a Business Structure?

A business structure is the legal form your venture takes — how it is owned, who bears its liabilities, how it is taxed, and what it must file each year. In India, the common forms are sole proprietorship, partnership firm, LLP, one person company (OPC), private company, and public company, governed mainly by the Indian Partnership Act, 1932, the Limited Liability Partnership Act, 2008, and the Companies Act, 2013.

The structure you pick is the first real decision of your business, because changing it later means transferring assets, contracts, and registrations to a new entity. Setindiabiz process experts weigh your liability exposure, funding plan, ownership, and compliance appetite against each form, then handle the filing of SPICe+ for companies, FiLLiP for LLPs, and a registered deed for partnerships once you decide.

Pradeep Vallat

Founder "Autonomo""Setindiabiz’s knowledgeable, disciplined, and organized team made our company registration, tax, and IPR filings smooth, hassle-free, and worry-free."

Popular Six Structures at a Glance

Before comparing them line by line, here is what each structure is and the kind of founder it suits. Each card names the governing law and the single most important feature — liability, ownership, or scale — that usually drives the choice. The detailed comparison matrix immediately after this section puts these side by side on the factors that matter most for a real decision.

Sole Proprietorship

One individual owns and runs the business; there is no separate legal entity, so the owner is personally liable for all debts. No dedicated statute and no MCA registration — only the tax and local licences the activity needs. Best for: solo traders, freelancers, and small local businesses testing an idea.

Read More

Partnership Firm

Two or more partners run a business under a partnership deed, governed by the Indian Partnership Act, 1932. Liability is unlimited and joint; registration is optional but practically essential (Section 69). Best for: small, trust-based businesses among known partners.

Read More

Limited Liability Partnership (LLP)

A body corporate under Section 3 of the LLP Act, 2008, combining a company's limited liability with a partnership's flexible internal management through the LLP agreement. Best for: professional firms and service businesses that don't need equity funding.

Read More

One Person Company (OPC)

A private company with a single member and a nominee, under Section 2(62) of the Companies Act, 2013. Gives a solo founder limited liability and corporate status. Best for: solo founders who want a company, not a proprietorship.

Read More

Private Company

A separate legal entity under the Companies Act, 2013, with limited liability, restricted share transfer, and a 200-member cap (Section 2(68)). The default choice for fundable, scalable startups. Best for: startups raising equity, issuing ESOPs, or planning to scale.

Read More

Public Company

A company that can invite public subscription to its securities, with a minimum of 7 members and no maximum (Section 2(71), Companies Act, 2013). Carries the heaviest governance and disclosure load. Best for: large ventures and businesses planning to raise capital from the public.

Read More

A solo founder who wants corporate status but not a full company can also consider a Hindu Undivided Family (HUF) for family businesses, or a Section 8 Company for not-for-profit objectives.

Sole Proprietorship vs Partnership vs LLP vs Private Company

Indian entrepreneurs have multiple pathways to structure their business ventures, with prevalent options including Sole Proprietorship, Partnership Firm, Limited Liability Partnership, and Private Limited Company. These structures are governed by specific laws, including the Indian Partnership Act, 1932; the LLP Act, 2008 (as amended in 2021); and the Companies Act, 2013. Each offers a unique balance of liability protection, regulatory compliance, operational costs, and business flexibility. A comprehensive comparison of these options is crucial for making an informed decision when formalising a business structure.

| Feature | Sole Proprietorship | Partnership Firm | Limited Liability Partnership (LLP) | Private Limited Company |

|---|---|---|---|---|

| Legal Status | No separate legal entity from the owner | Not separate from partners | Body corporate with separate legal entity (Section 3, LLP Act) | Separate legal entity (Section 9, Companies Act) |

| Governing Act | No specific act; general laws apply | Indian Partnership Act, 1932 | Limited Liability Partnership Act, 2008 | Companies Act, 2013 |

| Minimum Members | 1 (Owner) | 2 Partners (Section 4) | 2 Partners (Section 6) | 2 Shareholders (Section 3) |

| Maximum Members | 1 (Owner only) | 50 Partners (as per Companies Rules, 2014) | No limit ♾️ | 200 Shareholders (Section 2(68)) |

| Liability | Unlimited personal liability | Unlimited joint liability | Limited to capital contribution | Limited to the unpaid share value |

| Registration | No formal registration | Optional but recommended | Mandatory with ROC | Mandatory incorporation |

| Transfer of Ownership | Not transferable | Requires unanimous consent | As per the LLP Agreement | Share transfer (with restrictions) |

| Best For | Solo entrepreneurs, small traders | Small businesses with trusted partners | Professional services, medium businesses | Startups seeking funding, scaling up |

Timeline for Company / LLP Incorporation

Prep & name approval

Digital Signatures (DSC) for all directors/partners and name reservation via SPICe+ Part A (companies) or FiLLiP (LLP).

Document drafting

Drafting the MOA & AOA (companies) or the LLP agreement, plus subscriber and KYC documents.

Form submission

Filing the incorporation application — SPICe+ Part B with linked forms, or FiLLiP — with the MCA and paying the fees.

Scrutiny & incorporation

The Registrar of Companies (ROC) reviews the forms; upon approval, the Certificate of Incorporation is issued with the CIN/LLPIN, PAN, and TAN.

This timeline applies to the company and LLP routes. A sole proprietorship needs no MCA filing — it starts as soon as the required tax and local registrations are in place — and a partnership firm is set up on execution of the deed, with registration with the Registrar of Firms following separately.

Process: How Setindiabiz Helps You Choose and File

Choosing a structure and then registering it are two distinct stages, and we keep them separate so you can make a decision with full information before anything is filed. The five steps below cover the fullest route (a company or LLP); a proprietorship or partnership collapses the latter filing steps into a shorter registration path. Statutes referenced inline tell you exactly which rule governs each step.

Step 01: Map your ownership and liability profile.

First, we understand who owns and manages the business, and how much personal risk you want to keep off the table. We line your answers up against all six structures so the shortlist is built on your real model, not a template.

🕒 Turnaround: Same day after details are receivedStep 02: Shortlist structures against your growth plan.

Now we test your capital, funding intent, control preference, and scale against the shortlist, and explain the tax and compliance trade-offs of each — including the current Income-tax Act, 2025 position so the numbers are right.

🕒 Turnaround: 1 working dayStep 03: Confirm the route and document set.

Once the structure is chosen, we identify the filing route — SPICe+ for companies, FiLLiP for LLPs, or a registered deed for partnerships — and provide you with a precise document checklist, including KYC and office proof.

🕒 Turnaround: 1–2 working daysStep 04: Prepare and review the filing drafts.

We draft the core documents for the chosen form — MOA/AOA, LLP agreement, or partnership deed — and walk you through them before anything is submitted, so the constitution matches what you agreed to.

🕒 Turnaround: 1 working day after document clarityStep 05: File and hand over the registration.

We file with the relevant authority, track the application, and respond to any clarification. On approval,l you receive the Certificate of Incorporation (CIN/LLPIN) with PAN and TAN, and we guide you on the immediate next steps — bank account, GST, and licences.

🕒 Turnaround: Subject to authority processing (see Timeline)Why businesses trust us

Tax Rate of sole Proprietorship

A sole proprietorship is not a separate taxpayer; its income is added to the proprietor’s personal income and taxed at individual slab rates. The slabs below are for an individual resident below 60 years. The new tax regime (Section 115BAC) is the default; the old regime stays available as an option. Budget 2026 left the slabs unchanged, so FY 2025-26 (taxed under the Income-tax Act, 1961) and FY 2026-27 (taxed under the Income-tax Act, 2025) retain the same rates.

New tax regime (default) — resident individual below 60

| No | Income slab | FY 2025-26 (AY 2026-27) | FY 2026-27 (AY 2027-28) |

|---|---|---|---|

| 1 | Up to ₹4,00,000 | Nil | Nil |

| 2 | ₹4,00,001 – ₹8,00,000 | 5% | 5% |

| 3 | ₹8,00,001 – ₹12,00,000 | 10% | 10% |

| 4 | ₹12,00,001 – ₹16,00,000 | 15% | 15% |

| 5 | ₹16,00,001 – ₹20,00,000 | 20% | 20% |

| 6 | ₹20,00,001 – ₹24,00,000 | 25% | 25% |

| 7 | Above ₹24,00,000 | 30% | 30% |

Old tax regime (optional) — resident individual below 60

| No | Income slab | FY 2025-26 (AY 2026-27) | FY 2026-27 (AY 2027-28) |

|---|---|---|---|

| 1 | Up to ₹2,50,000 | Nil | Nil |

| 2 | ₹2,50,001 – ₹5,00,000 | 5% | 5% |

| 3 | ₹5,00,001 – ₹10,00,000 | 20% | 20% |

| 4 | Above ₹10,00,000 | 30% | 30% |

On top of the slab tax, a 4% health and education cess applies in both years, and a surcharge applies at higher incomes (from 10% above ₹50 lakh, capped at 25% under the new regime). Under the new regime, a Section 87A rebate makes taxable income up to ₹12,00,000 effectively tax-free; under the old regime, the rebate covers income up to ₹5,00,000. The old regime gave a higher basic exemption to senior citizens (60–80: ₹3,00,000) and super-senior citizens (80+: ₹5,00,000); those are not shown here, as this table assumes a proprietor below 60.

Tax Rate of Limited Liability Partnership (LLP)

An LLP, like a partnership firm, is taxed as a firm, not at slab rates: a flat 30% on total income, however small or large, under the Income-tax Act, 2025 (the Income-tax Act, 1961 for FY 2025-26). The table below sets out every component so the effective rate is fully worked out, with no figure left to infer.

| No | Total income | Base rate | Surcharge | Health & Education Cess | Effective rate |

|---|---|---|---|---|---|

| 1 | Up to ₹1 crore | 30% | Nil | 4% (on tax) | 31.20% |

| 2 | Above ₹1 crore | 30% | 12% (on tax) | 4% (on tax + surcharge) | 34.94% |

A firm and an LLP are taxed identically — the flat 30% applies from the first rupee of profit, surcharge is added only once income crosses ₹1 crore, and the 4% cess is applied last on tax plus surcharge. Two further points complete the picture: where the LLP/firm claims certain deductions, the Alternate Minimum Tax of 18.5% of adjusted total income applies (Section 115JC), and where income only marginally exceeds ₹1 crore, marginal relief caps the surcharge so the extra tax cannot exceed the extra income.

Tax Rate of the Company

A company — whether an OPC, a private company, or a public company is taxed as a domestic company under the Income-tax Act, 2025, not at individual slab rates. Its rate depends on the regime it chooses and, in the normal regime, on its income band. The table sets out every component for each combination, with the effective rate worked out; the following footnotes explain the 115BAA and 115BAB concessional regimes and MAT.

Normal Tax Rate on Companies

| No | Regime and income band | Base rate | Surcharge | Health & Education Cess | Effective rate |

|---|---|---|---|---|---|

| 1 | Turnover ≤ ₹400 crore, income up to ₹1 crore | 25% | Nil | 4% | 26.00% |

| 2 | Turnover ≤ ₹400 crore, income ₹1–10 crore | 25% | 7% | 4% | 27.82% |

| 3 | Turnover ≤ ₹400 crore, income above ₹10 crore | 25% | 12% | 4% | 29.12% |

| 4 | Turnover > ₹400 crore, income up to ₹1 crore | 30% | Nil | 4% | 31.20% |

| 5 | Turnover > ₹400 crore, income ₹1–10 crore | 30% | 7% | 4% | 33.38% |

| 6 | Turnover > ₹400 crore, income above ₹10 crore | 30% | 12% | 4% | 34.94% |

Concessional Tax Rate Under section 115BAA/115BAB

| No | Regime and income band | Base rate | Surcharge | Health & Education Cess | Effective rate |

|---|---|---|---|---|---|

| 1 | Section 115BAA (any income) | 22% | 10% | 4% | 25.17% |

| 2 | Section 115BAB, new manufacturing (CLOSED) | 15% | 10% | 4% | 17.16% |

Notes to the company tax table

- Section 115BAA (22% concessional rate): Any domestic company may opt for this regime. It carries a flat 10% surcharge at every income level plus 4% cess, giving an effective rate of 25.17%. In return, the company gives up specified deductions and incentives (such as SEZ benefits, additional depreciation, and most Chapter VI-A claims, other than Sections 80JJAA and 80M). Once opted, the choice is irreversible, and the company is taken outside MAT. (Section 115BAA of the Income-tax Act, 1961, carried forward under the Income-tax Act, 2025; opted in by filing Form 10-IC before the return is due.)

- Section 115BAB (15% new-manufacturing rate) — Closed Now. This 15% rate (effective 17.16% with the flat 10% surcharge and 4% cess) was available only to a new domestic manufacturing company set up on or after 1 October 2019 that commenced manufacturing on or before 31 March 2024. That sunset date was not extended, so the rate is closed to new entrants and is shown here only for completeness. Companies that are already validly under it are also outside MAT.

- Minimum Alternate Tax (MAT). A company in the normal regime (the 25% and 30% rows above) pays MAT at 15% of book profit, plus surcharge and 4% cess, whereas its normal tax works out to be lower than that (Section 115JB). MAT does not apply to companies that opt for the 115BAA or 115BAB concessional regimes — that exemption is one of the main reasons the concessional regimes are attractive.

- The base rate is 25% only where the company’s turnover in the prescribed prior year did not exceed ₹400 crore; otherwise, it is 30%. The same marginal relief principle applies at the ₹1 crore and ₹10 crore surcharge thresholds, capping the surcharge so the extra tax cannot exceed the extra income.

- DPIIT-recognised startups (companies or LLPs) may claim a profit-linked tax holiday for three consecutive years out of their first ten under Section 80-IAC — see the DPIIT 80-IAC tax exemption page for the current eligibility window.

How to Choose Your Structure

No “best” structure exists—only the one fitting your risk, capital, and control needs. Evaluate your business through these five filters, each mapping to statutory outcomes rather than mere preference. If filters conflict, prioritise the one with the highest long-term cost or risk, and consult a Setindiabiz expert before filing.

Evaluate Liability exposure.

If a business setback could reach your personal home, car, or savings, pick a limited-liability form — LLP, OPC, private, or public company — where the entity is legally separate from you (Section 3, LLP Act, 2008; Section 9, Companies Act, 2013). Proprietorship and partnership leave personal assets exposed.

Future Funding plan.

If you expect angel or VC investment, share classes, or ESOPs, choose a private company — only a share-based entity supports equity dilution and clean exits (Section 2(68) of the Companies Act, 2013). Self-funded businesses can stay simpler.

What about Controlling the startups.

Want full solo control? One person owns a proprietorship (OPC). Sharing control with co-founders suggests a partnership or an LLP; a company separates ownership (shareholders) from management (the board).

Scale and continuity.

A separate entity with perpetual succession (LLP, OPC, company) survives the death, exit, or transfer of an owner; a proprietorship or partnership does not. Choose accordingly if the business must outlast its founders.

Tax and compliance appetite.

A proprietorship has the lightest compliance burden and is taxed at your slab rate; firms and LLPs pay a flat 30%; companies access the 25%/22% tax rates but require annual ROC filing and audit. Weigh the rate against the filing load you can sustain.

Related Reading

Frequently Asked Questions

It is the legal form your venture takes — proprietorship, partnership, LLP, OPC, private company, or public company. The form decides your liability, taxation, ownership, and the filings you must make each year, and is governed mainly by the Indian Partnership Act, 1932, the LLP Act, 2008, and the Companies Act, 2013.

A sole proprietorship is the easiest — there is no dedicated Act and no MCA registration, only the tax and local licences your activity needs. It is the fastest way for a solo trader to begin, though the owner carries unlimited personal liability for the firm’s debts.

The decisive difference is liability. In a partnership firm under the Indian Partnership Act, 1932, partners have unlimited joint liability, exposing their personal assets. An LLP is a body corporate under Section 3 of the LLP Act, 2008, where each partner’s liability is limited to the agreed contribution.

An OPC is a private company with one member and a nominee (Section 2(62), Companies Act, 2013). Unlike a proprietorship, it is a separate legal entity with limited liability and perpetual succession, while a proprietorship has no legal separation from its owner.

A private company (Section 2(68)) restricts share transfers, caps the number of members at 200, and cannot invite public subscription. A public company (Section 2(71)) needs at least 7 members, has no member cap, and may raise capital from the public, with heavier governance and disclosure obligations.

One person can run a proprietorship or an OPC. A partnership and an LLP need at least 2 (Section 6, LLP Act). A private company needs 2 members and 2 directors; a public company needs 7 members and 3 directors (Companies Act, 2013).

An OPC requires the member and nominee to be Indian citizens, so foreigners cannot use it; NRIs who are Indian citizens may use it after the 2021 reforms. LLPs and companies accept foreign investment, subject to the FDI policy and FEMA, and need at least one resident director or designated partner.

A partnership firm is limited to 50 partners (Rule 10 of the Companies (Miscellaneous) Rules, 2014). An LLP has no maximum (Section 6, LLP Act). A private company is capped at 200 members (Section 2(68)), excluding present and former employee-shareholders; a public company has no cap.

No. The Companies Act, 2013 (as amended in 2015) removed the minimum paid-up capital requirement for both private and public companies, so that you can incorporate with the capital your business actually needs and increase it later.

A company must have at least one director who stayed in India for 182 days or more in the previous financial year (Section 149(3)). An LLP must have at least one designated partner resident in India, with residency measured at 120 days (LLP (Amendment) Act, 2021).

A private company. Investors prefer it because it allows for equity dilution, multiple share classes, ESOPs, and defined exits (Section 2(68) of the Companies Act, 2013). Proprietorships, partnerships, and OPCs cannot issue shares to outside equity investors.

A sole proprietorship — no MCA annual filing and no statutory audit, only tax and local registrations. LLPs file Form 8 and Form 11 each year; companies file annual ROC returns and undergo statutory audits, so their compliance burden is higher.

Choose an LLP for flexible, partner-led management and lower compliance where you do not need outside equity. Choose a private company where shareholding, investors, ESOPs, or rapid scaling are central — its share-based structure is built for funding and growth.

Yes — a proprietorship or partnership can be converted into an LLP or a private company, and an OPC into a private or public company at any time (the earlier two-year wait was removed in 2021). Conversion affects assets, contracts, and taxes, so it is best to choose with the plan in mind.

LLPs (Section 3, LLP Act), OPCs, and private and public companies (Section 9, Companies Act, 2013) all continue regardless of changes in ownership, whether by death, retirement, or transfer. A proprietorship and a partnership do not have this continuity.

KYC of the directors/partners (PAN, Aadhaar, ID and address proof), passport-size photos, registered-office proof with an NOC, and a Digital Signature for each signatory. Companies also need a drafted MOA and AOA; LLPs need the LLP agreement.

Yes. A residential address can be the registered office of a company or LLP, provided you submit a No Objection Certificate from the owner and a recent utility bill as proof of address.

It is optional under the Indian Partnership Act, 1932, but strongly advised. An unregistered firm cannot sue to enforce a contractual right or claim set-off (Section 69), which is a serious disadvantage in practice, so most firms register with the Registrar of Firms.

A private or public company is required to have a statutory audit by a Chartered Accountant every year, regardless of turnover (Companies Act, 2013). An LLP needs an audit only if turnover exceeds ₹40 lakh or contribution exceeds ₹25 lakh in a financial year.

The owner runs a proprietorship; partners run a partnership and an LLP, with designated partners accountable for LLP compliance (Section 8, LLP Act). In a company, the board manages while shareholders own — the two roles are separate.

A proprietorship is taxed in the owner’s hands at individual slab rates. Partnership firms and LLPs pay a flat 30% plus surcharge and cess. Companies pay 30% by default, 25% if turnover is ≤ ₹400 crore, or 22% under the concessional regime — all under the Income-tax Act, 2025, for Tax Year 2026-27 onward.

No. The 15% rate for new manufacturing companies (Section 115BAB) required manufacturing to commence on or before 31 March 2024, and that window was not extended. New companies should plan around the 22% concessional rate as the lowest rate generally available to companies.

DPIIT-recognised startups can claim a profit-linked tax holiday for three consecutive years out of their first ten under Section 80-IAC, subject to conditions. This benefit is generally available to eligible companies and LLPs — see the DPIIT 80-IAC page for the current eligibility window.

Once turnover crosses ₹40 lakh (goods) or ₹20 lakh (services), or where a Section 24 trigger applies (inter-state supply, e-commerce, reverse charge), GST registration is compulsory, whichever structure you choose. Under GST 2.0, the slabs are 5% and 18%, with a simplified route under Rule 14A.

A small company is a private company with paid-up capital ≤ ₹4 crore and turnover ≤ ₹40 crore (Companies (Specification of Definitions Details) Amendment Rules, 2022). The status offers lighter compliance requirements, but it does not apply to holding/subsidiary companies or Section 8 companies.

Setindiabiz is Trusted By Leading Brands