Start Your Business in India | We help you do right!

Starting a business in India begins with choosing the right legal structure, filing it, and obtaining the registrations you need to operate. Setindiabiz process experts guide Indian and foreign founders from that first decision to a compliant, running business.

🗹 Key Information of Start Your Business |

||

|---|---|---|

| 1 | First thing to decide | Your legal structure drives liability, tax, funding, and compliance. |

| 2 | Timeline |

|

| 3 | Cost | Government fees on actuals (state stamp duty/ROC fees vary); professional fee quoted upfront. |

| 4 | For Indian founders | Any Indian citizen aged 18+ |

| 5 | For NRI / OCI | Can hold shares/be directors in companies and LLPs (FDI route); a proprietorship only on a non-repatriation basis under Schedule 4, FEM (Non-Debt Instruments) Rules, 2019. |

| 6 | For Foreigners | Usually via an Indian Private Limited Company or LLP under the FDI policy and FEMA, with FC-GPR reporting to the RBI. A proprietorship is not available. |

| 7 | Liability | At least one director resident in India ≥182 days in the financial year (Section 149(3), Companies Act, 2013) |

| 8 | Resident director (companies) | Optional but useful: a notarised brand-adoption affidavit or a newspaper notice fixes the date of first use under Section 34, Trade Marks Act, 1999; a trademark application gives full registered rights. |

| 9 | After setup | PAN, TAN, current account, and registrations such as GST, IEC, FSSAI, Shops & Establishment, Professional Tax, EPFO/ESIC, as applicable. |

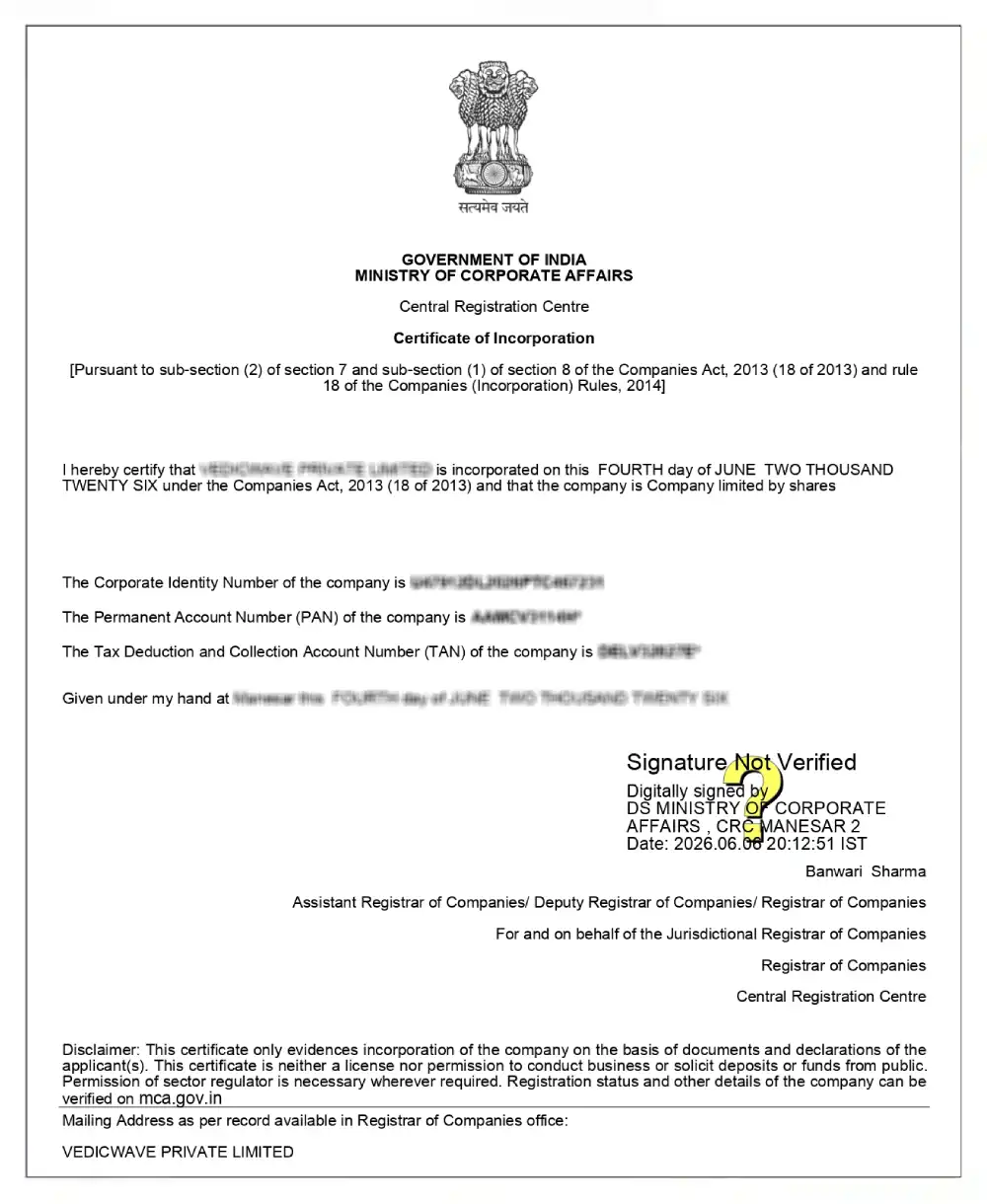

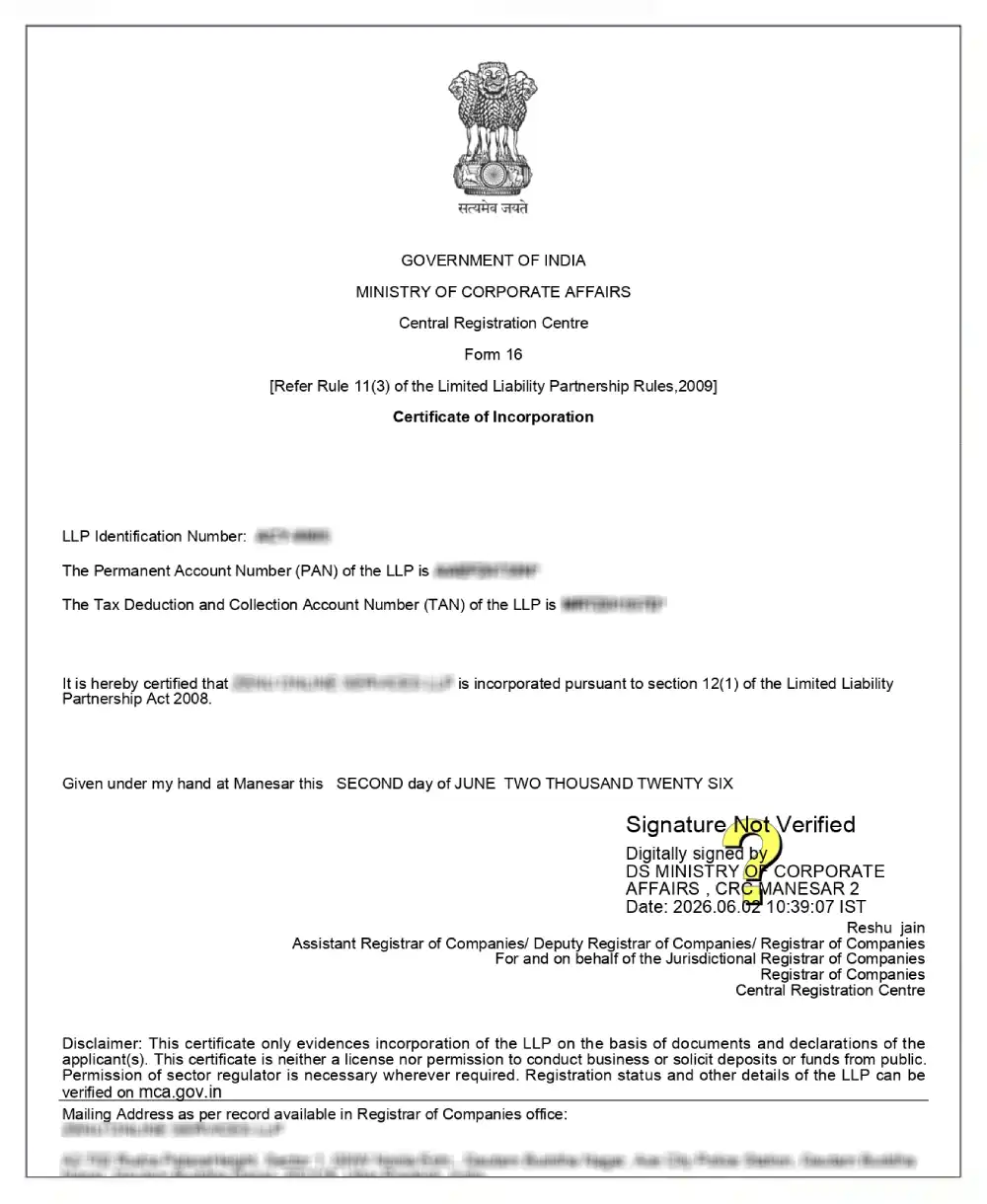

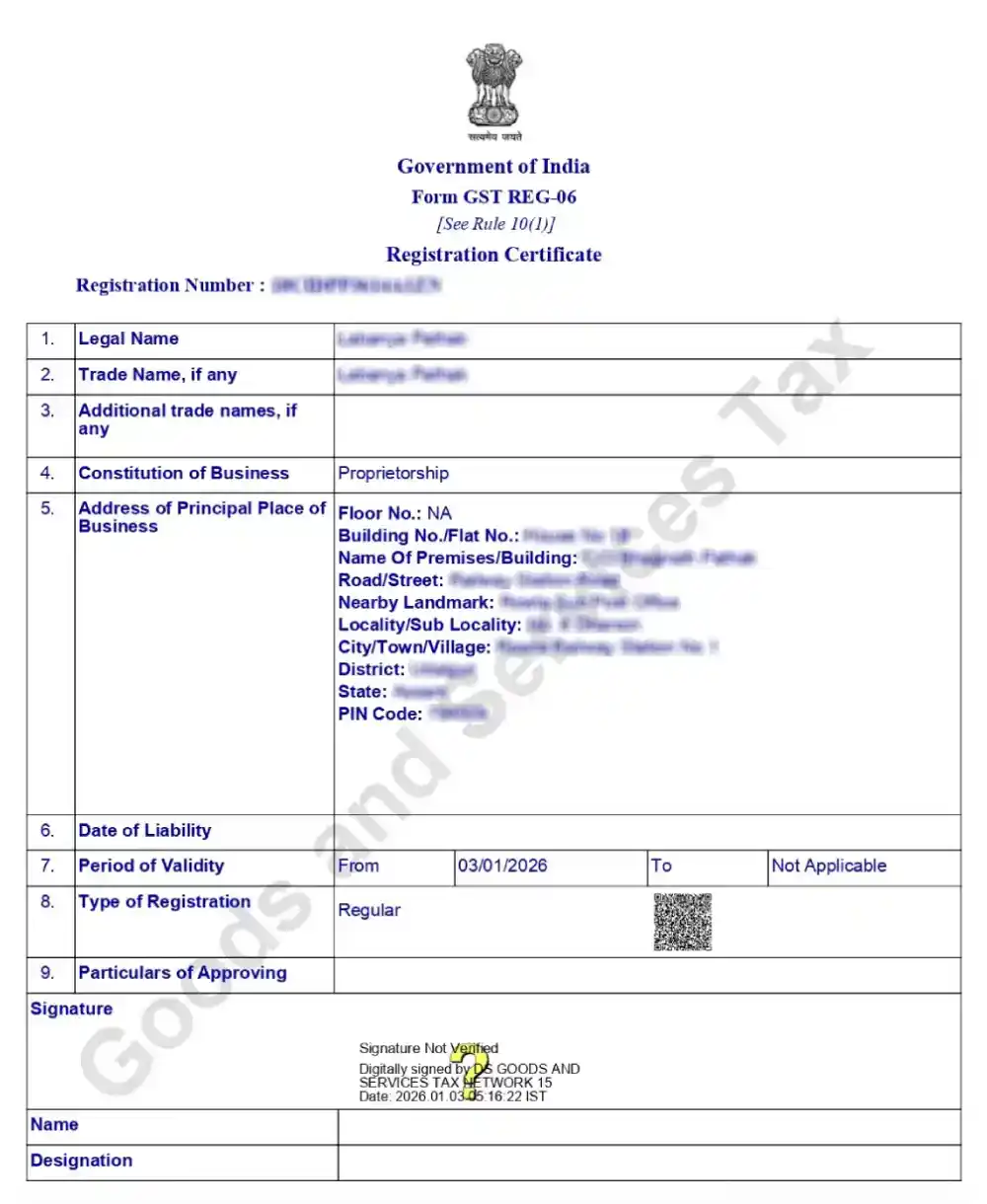

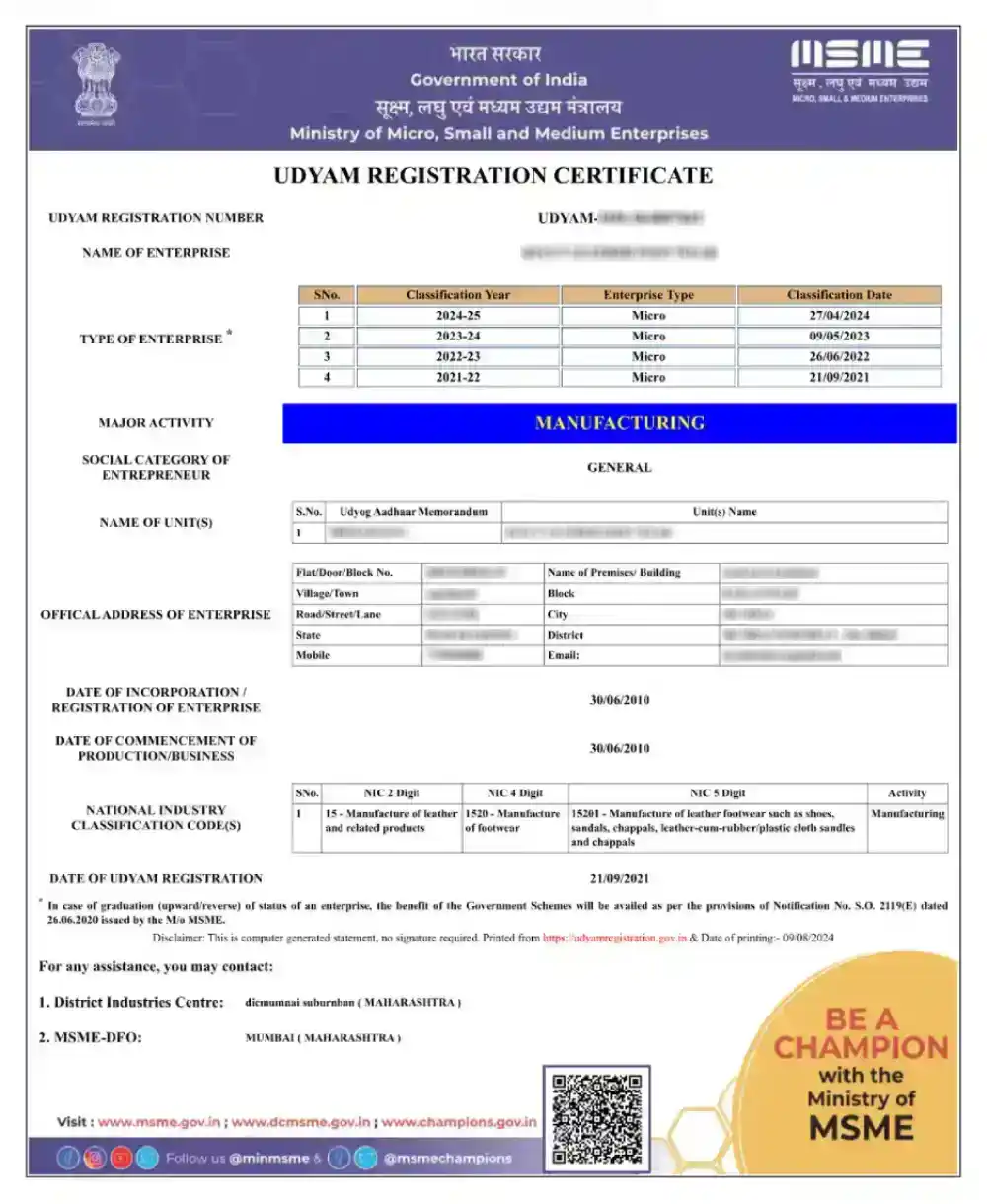

COI of Company + COI of LLP + GST Certificate + MSME + Trademark

What does it mean to start a business in India?

Starting a business in India means choosing a legal structure, such as a Private Limited Company, LLP, OPC, partnership, proprietorship, or Section 8 Company, and completing the filings that bring it into existence under the Companies Act, 2013, the LLP Act, 2008, or the Indian Partnership Act, 1932. The structure you pick shapes your liability, tax, funding, and ongoing compliance, so it is the first real decision.

It rarely ends at incorporation. Most founders also need PAN, TAN, a current account, and registrations such as GST, IEC, FSSAI, or Shops & Establishment before they can invoice. Setindiabiz helps you choose the structure, prepare documents, file the application, and add the right registrations at the right stage.

Pradeep Vallat

Founder "Autonomo""Setindiabiz’s knowledgeable, disciplined, and organized team made our company registration, tax, and IPR filings smooth, hassle-free, and worry-free."

Most Popular Business Types in India

The structure you choose is the foundation of everything that follows — how you are taxed, whether your liability is limited, how easily you can raise funding, and how much annual compliance you carry. The summary below points you to the right-fit option; for a full feature-by-feature comparison of taxation, ownership, and compliance, use the dedicated business structure comparison page before you commit.

Private Limited Company

This is the most preferred structure for startups and growing businesses. Attracts investors easily, enables equity funding, and offers credibility—a separate legal entity with limited liability and perpetual succession benefits.

Read More

Limited Liability Partnership

Modern hybrid structure combining partnership flexibility with corporate-style limited liability protection. Lower compliance than companies. Preferred by professionals like CAs, lawyers, and consulting firms.

Read More

One Person Company (OPC)

Revolutionary single-member company structure with limited liability benefits and separate legal entity status. Enables solo entrepreneurs to enjoy corporate advantages while maintaining complete ownership control.

Read More

Section 8 Company

Non-profit company structure for charitable, educational, social, and religious objectives. Enjoys tax exemptions and government grants. Profits reinvested for social causes, not distributed to members.

Read More

Sole Proprietorship

Single-owner business with complete control over operations and decision-making. Simplest structure with minimal compliance but unlimited personal liability. Ideal for small-scale individual ventures and consultants.

Read More

Partnership Firm

Two or more partners jointly manage a business, sharing in its profits and losses and assume unlimited liability. Governed by the Partnership Act 1932. Perfect for professional services requiring combined expertise and shared resources.

Read More

Eligibility / Minimum Requirements

Most structures share a short set of baseline requirements, with a few that apply only to companies. These are worth confirming before you file, because a missing resident director or an unproven registered office is the most common reason an otherwise-ready application stalls. The criteria below cover the common case; the entity pages linked above carry the structure-specific detail.

Capacity to contract.

Every founder, director or partner must be competent to contract under Section 11 of the Indian Contract Act, 1872, of majority age and sound mind.

Resident director (companies).

At least one director must have stayed in India for not less than 182 days during the financial year — Section 149(3), Companies Act, 2013.

Minimum members.

A Private Limited Company needs 2–200 shareholders; an OPC needs one member; an LLP needs at least two designated partners; a partnership needs two or more partners.

Unique name.

The proposed name must not be identical or too similar to an existing company or trademark, per the Companies (Incorporation) Rules, 2014.

Registered office.

A company must maintain a registered office for statutory communication within 30 days of incorporation — Section 12, Companies Act, 2013. A residential address is acceptable with a utility bill and the owner's NOC.

No minimum capital (companies).

No statutory floor since the Companies (Amendment) Act, 2015 — start with any amount and maintain working capital to operate.

Lawful object.

The business objects must be legal; regulated activities (food, drugs, finance) require their own licence before operations begin.

Timeline for Starting a Business in India

Plan & documents

We confirm your structure and collect founder KYC, office proof, and business details.

Name & drafts

DSC for directors; name reservation via SPICe+ Part A; entity-specific drafts (e-MOA / e-AOA for companies).

Entity filing

We file the incorporation application (SPICe+ Part B for companies; FiLLiP for LLP) and track authority review.

Tax & operating setup

PAN, TAN, current account, and GST / other registrations aligned, plus your first compliance actions.

A proprietorship is faster (same-day to about a week); a company sits at the longer end. Timelines vary with name approval and authority review.

Process to Start a Business in India

Starting a business is a sequence, not a single filing, and the order matters — structure first, documents next, then the entity, then the registrations that let you trade. We run the steps below and keep you updated at each stage; simpler structures (a proprietorship trading in its own name) collapse steps 3 and 4. The functional lines on each card show what we need from you and the working-day turnaround.

Step 01: Choose the right structure for your plan.

We start with your ownership, funding plan, comfort with liability, tax position, and compliance appetite, then shortlist the structure that actually fits — rather than defaulting every founder to the same entity.

⏳ Turnaround: Same day after consultation

Step 02: Collect founder and office documents.

We collect KYC, proof of registered office, ownership or rental papers, and the owner’s NOC. For foreign founders, we flag notarisation, apostille or consularisation before drafting starts.

⏳ Turnaround: 1–2 working days after complete documents

Step 03: Reserve the name and prepare a draft.

We run a practical name check against the MCA portal and the trademark registry under the Companies (Incorporation) Rules, 2014, align the object clause with your activity, and prepare structure-specific drafts — SPICe+, e-MOA (INC-33), and e-AOA (INC-34) — for a company.

⏳ Turnaround: 1–2 working days after name clarity

Step 04: File with the authority.

Once drafts are approved, we file the application — SPICe+ Part B with AGILE-PRO-S for a company, FiLLiP for an LLP — respond to any clarification, and track it to the Certificate of Incorporation.

⏳ Turnaround: 3–6 working days, subject to review

Step 05: Add tax and operating registrations.

After the entity exists, we assess and file what you actually need — GST (turnover or Section 24 triggers; Rule 14A where eligible), IEC, FSSAI, Shops & Establishment, Professional Tax, EPFO/ESIC, or DPIIT recognition.

⏳ Turnaround: 2–5 working days per registration

Step 06: Start your first compliance calendar.

We set up your opening compliance checklist — for a company: the INC-20A commencement filing, first auditor appointment, statutory registers, GST returns, and annual filings — so you can start operating without missing early obligations.

⏳ Turnaround: Same day after the registration output

Why businesses trust us

Registrations You May Need After Setup

Incorporation gives you a legal entity, not a fully operational business. Before you can invoice, bank and hire, a different set of registrations usually applies, driven by your activity, turnover, state and headcount rather than your structure. Some attach at incorporation through the integrated SPICe+ / AGILE-PRO-S form; others are taken when the trigger is hit. The table maps the common registrations.

| Registration | When it applies | Statutory hook |

|---|---|---|

| PAN & TAN | Tax identity, TDS, banking and statutory filings — allotted with company/LLP incorporation. | Income-tax Act, 1961 (Tax Year 2026-27 onwards: Income-tax Act, 2025) |

| GST registration | Turnover above ₹40 lakh (goods) / ₹20 lakh (services), or from the first transaction under Section 24, triggers inter-state supply, e-commerce, or reverse charge. Small taxpayers can opt for Rule 14A simplified registration. | CGST Act, 2017; Section 24; Rule 14A, CGST Rules, 2017 |

| Import Export Code (IEC) | Any import or export of goods/services. | Foreign Trade (Development & Regulation) Act, 1992 (DGFT) |

| FSSAI | Before starting any food business. | FSS Act, 2006 [VERIFY: confirm FSSAI registration slug] |

| Shops & Establishment | Commercial establishments, under the relevant State Act. | State Shops & Establishments Acts |

| Professional Tax | In states that levy professional tax. | State Professional Tax Acts |

| EPFO & ESIC | On crossing the statutory employee thresholds, they can be linked at incorporation for companies via AGILE-PRO-S. | EPF & MP Act, 1952; ESI Act, 1948 [VERIFY: confirm PF registration slug] |

| MSME (Udyam) | Optional but useful — a free certificate in the firm’s name, accepted by banks and for government benefits. | MSMED Act, 2006 |

Private Limited Company vs LLP: Which Suits You?

Selecting between a Private Limited Company and a Limited Liability Partnership (LLP) significantly impacts funding capabilities, compliance requirements, taxation structure, and operational flexibility. This comprehensive comparison helps you understand the fundamental differences to determine your ideal business framework. Let me break down each aspect to help you make an informed decision that aligns with your business goals and growth strategy.

| No | Feature | Private Limited Company | Limited Liability Partnership |

|---|---|---|---|

| 1 | Governing Act | Governed by the Companies Act, 2013, which mandates stricter compliance requirements and detailed regulations | Governed by the Limited Liability Partnership Act, 2008, offering greater operational flexibility and simplified procedures |

| 2 | Legal Status | ✅ Separate legal entity, utterly distinct from its shareholders, with independent existence | ✅ Separate legal entity, entirely distinct from its partners, with independent legal recognition |

| 3 | Ownership Structure | Owned by 2 to 200 shareholders – ideal for distributing equity and structured ownership | Owned by a minimum of 2 partners with no upper limit – perfect for professional collaborations |

| 4 | Fundraising Capability | ✅ Most preferred structure for raising capital from Angel Investors, VCs, banks, and the public | Limited to partner contributions and loans from financial institutions – equity funding restricted |

| 5 | Transfer of Ownership | ✅ Effortless – ownership transferred by just transferring shares to another person | ❌ Complex process requiring unanimous consent of all existing partners for any transfer |

| 6 | Compliance Burden | Higher – Mandatory board meetings, Annual General Meetings (AGM), annual filings (AOC-4, MGT-7) | Lower – No mandatory meetings required; audit only if turnover exceeds ₹40 Lakhs annually |

| 7 | Meeting Requirements | Minimum four board meetings yearly, 1 AGM mandatory within 6 months of the financial year end | No statutory meeting requirements – partners decide meeting frequency based on business needs |

| 8 | Taxation Structure | 💰 Lower effective rate: 22%-25% (plus cess) under the new tax regime – more tax efficient | 30% flat rate (plus surcharge and cess) on profits – higher tax burden for profitable ventures |

| This comparison reveals that while Private Limited Companies excel in fundraising and growth potential, with lower taxation, LLPs offer operational simplicity and flexibility, along with reduced compliance. Your choice should align with your long-term business vision, funding requirements, and appetite for regulatory compliance. Setindiabiz helps you navigate this crucial decision with expert guidance tailored to your specific business needs! | |||

Frequently Asked Questions

Start by choosing the right legal structure, because it determines your liability, taxes, funding, and compliance. Then file the entity and add the registrations your activity needs. The structure decision is the one worth getting right first.

A Private Limited Company is usually preferred for startups planning equity funding, ESOPs and structured ownership under the Companies Act, 2013. An LLP suits partner-led service firms that are not raising equity. Compare them on the business-structure page before deciding.

Yes. A proprietorship can be converted into an OPC, Private Limited Company, or LLP as it grows by incorporating a new entity and transferring the business. Conversion can involve tax, asset-transfer and licence steps, so choose the long-term structure early if funding or limited liability matters.

Choose an LLP for flexible, partner-led operations with lighter routine compliance and no equity-funding plan. Choose a Private Limited Company where structured shareholding, investor entry and scale matter. The trade-off is flexibility versus fundability.

Open a current account, complete tax registrations, set up accounting and invoicing, maintain statutory records, and start your compliance calendar. For a company, file INC-20A to commence business before operations begin.

Yes. Foreign nationals and companies can invest in or set up Indian entities — usually a Private Limited Company or LLP — under the FDI policy and FEMA, subject to sector rules, documentation, and FC-GPR reporting to the RBI. A proprietorship is not available to foreign nationals.

Only on a non-repatriation basis, under Schedule 4 of the FEM (Non-Debt Instruments) Rules, 2019. For repatriable investment, an NRI/OCI is generally better served by a company or LLP.

Yes. Under Section 149(3) of the Companies Act, 2013, at least one director must have stayed in India for not less than 182 days during the financial year. The board can otherwise include foreign nationals.

After a foreign investor subscribes to shares, the Indian company reports the allotment to the RBI in Form FC-GPR within the prescribed time. Setindiabiz handles the FEMA reporting alongside incorporation.

Yes, for companies. Section 12 of the Companies Act, 2013 requires a registered office for statutory communication within 30 days of incorporation. A residential address is acceptable with a utility bill and the owner’s NOC.

No. There has been no minimum paid-up capital requirement for a private company since the Companies (Amendment) Act, 2015. Start with any amount and maintain enough working capital to operate.

Yes, for online MCA filings. A DSC is mandatory for e-filing incorporation forms and is issued by licensed Certifying Authorities. We procure DSCs for all directors as part of the process.

The name must be unique and not identical or deceptively similar to an existing company or trademark, per the Companies (Incorporation) Rules, 2014. We run a name check against the MCA portal and the trademark registry before filing SPICe+ Part A.

About 8–12 working days for a company end-to-end, depending on document readiness, name approval and ROC review. A proprietorship can take from one day to about a week. Each added registration runs on its own short timeline.

SPICe+ is the integrated MCA V3 incorporation form. Part A reserves the name; Part B, filed with e-MOA (INC-33), e-AOA (INC-34) and AGILE-PRO-S, applies for incorporation, DIN, PAN, TAN, GSTIN and EPFO/ESIC in one submission.

Once turnover crosses ₹40 lakh for goods or ₹20 lakh for services (lower in special-category states), and from the first transaction under Section 24 triggers — inter-state supply, e-commerce, or reverse charge. Small taxpayers can opt for Rule 14A simplified registration.

Yes. Voluntary registration is useful for B2B billing, marketplace onboarding, or claiming input tax credit, even below the threshold. [VERIFY: confirm the latest GST portal advisory before publishing.]

Founder KYC (PAN, ID proof, address proof, photo), registered-office proof (utility bill, rent/ownership proof, NOC), and business details (names, objects, capital, ownership). Foreign founders may not need notarised or apostilled documents. [VERIFY: confirm the final list by entity type.]

It is optional but useful. Udyam registration under the MSMED Act, 2006, is free, provides a certificate in the firm’s name accepted by banks, and unlocks government benefits and easier access to credit.

It is the declaration for the commencement of business that a company with share capital must file before starting operations or borrowing. We file it as part of your first compliance steps.

The total is government fee on actuals (ROC fee and state stamp duty for companies; nil for Udyam/GST), third-party costs (DSC, attestation), and the Setindiabiz professional fee quoted upfront. [VERIFY: confirm package prices.]

A DPIIT-recognised Private Limited Company or LLP that obtains a separate IMB Certificate of Eligibility can claim a 100% profit deduction for any three consecutive years in its first ten, under Section 80-IAC, if incorporated before 1 April 2030. DPIIT recognition by itself does not grant the deduction.

No. Section 56(2)(viib) — the angel tax — was abolished with effect from 1 April 2025 (AY 2025-26) for all investor classes by the Finance (No. 2) Act, 2024. New funds that raise above fair market value no longer attract it.

A company is taxed as a separate entity; a proprietorship’s income is added to the proprietor’s personal income at slab rates. Income for FY 2025-26 is assessed under the Income-tax Act, 1961, and for Tax Year 2026-27 onwards under the Income-tax Act, 2025. The effective rate depends on entity type, income and the chosen regime.

Setindiabiz is Trusted By Leading Brands