The default rule in company law is one share, one vote. But the Companies Act, 2013, allows a company to break that symmetry and issue shares that carry more or fewer votes than their economic stake would suggest. Used well, differential voting rights help founders raise capital without surrendering control; used carelessly, they breach Rule 4 or SEBI norms. This guide explains who can issue DVR shares, the 74% voting cap, and how the rules differ for private, public and listed companies.

What DVR Shares Mean in Law

A differential voting rights share is still an equity share; it simply carries a different bundle of rights from an ordinary share, usually more dividends in exchange for fewer votes, or more votes in exchange for a smaller economic claim. Founders use them to raise money without handing control to incoming investors. The Companies Act, 2013 permits this departure from the plain equity share, but only inside a defined statutory frame, which is where Section 43 begins.

Under Section 43 of the Companies Act, 2013, the equity share capital of a company limited by shares may be of two kinds: shares with ordinary voting rights, or shares with differential rights as to dividend, voting or otherwise, issued in accordance with the prescribed rules.

That single clause is the legal source of every DVR share in India; it carves out a lawful exception to the “one share, one vote” default in Section 47 of the Companies Act, 2013, under which voting power normally tracks paid-up equity in exact proportion. DVR shares are how a company deliberately separates the right to vote from the right to a share of profit, so a founder can keep decision-making power even as ownership widens.

Can One Share Carry 10,000 Votes?

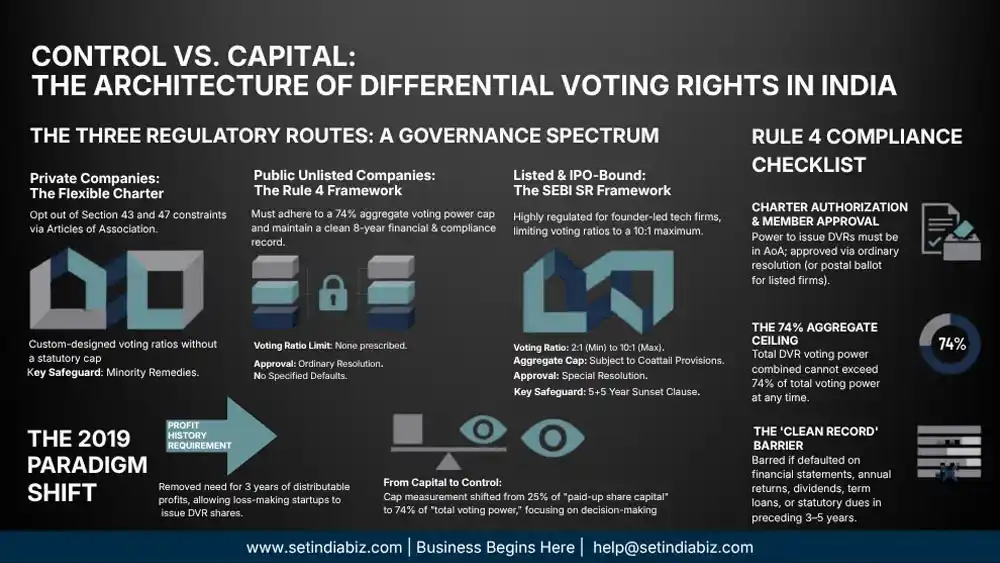

This is the question founders ask first, and the honest answer is that it depends on the company. The starting point under Section 47 is one vote per equity share, in proportion to paid-up capital, with DVR shares being the lawful exception. But how far that exception can stretch, whether a single share can carry ten, a hundred or ten thousand votes, turns entirely on whether the company is private, public or listed.

For an unlisted company governed by Rule 4, the law does not prescribe a fixed maximum votes-per-share ratio. What it caps is the aggregate: under Rule 4(1)(c) of the Companies (Share Capital and Debentures) Rules, 2014, the combined voting power of all DVR shares must not exceed 74% of the company’s total voting power. So an extreme ratio is not expressly forbidden, a 1:10,000 structure is conceivable in principle, but only if the total DVR voting power still sits inside that 74% ceiling, the articles authorise it, members approve it, and the structure is properly disclosed and commercially justified. For a listed company, the answer is firmer: SEBI caps the superior-voting ratio at 10:1, so a five-figure ratio is simply off the table.

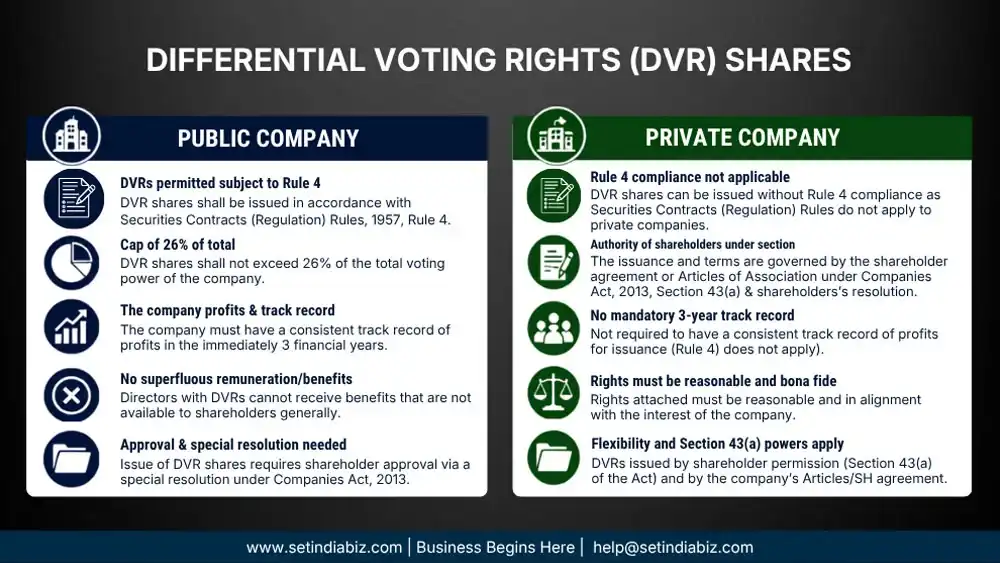

Public Companies: Rule 4

Rule 4 of the Companies (Share Capital and Debentures) Rules, 2014, is the gatekeeper for DVR shares. It binds every company limited by shares, a public limited company, listed or unlisted, and any private company that has not opted out of Section 43 through its charter. The rule does not ask whether a DVR issue is a good idea; it asks whether the company has cleared a fixed checklist of conditions before the shares can be issued at all.

Conditions under Rule 4(1) for DVR

| Rule | condition | What it means in practice |

|---|---|---|

| Rule 4(1)(a) | AOA must authorise | The power to issue DVR shares must already be set out in the articles of association; if it is not, the articles must first be amended by special resolution. |

| Rule 4(1)(b) | Shareholders Approval | Members approve the issue at a general meeting with an ordinary resolution |

| Rule 4(1)(c) | DVR voting power within 74% | The voting power of all DVR shares, taken together, cannot exceed 74% of the company’s total voting power at any point in time. |

| Rule 4(1)(e) | Clean filing record | No default in filing financial statements or annual returns for the three financial years immediately preceding the issue. |

| Rule 4(1)(f) | No subsisting payment defaults | No unpaid declared dividend, matured deposit, or redemption of preference shares or debentures that have fallen due. |

| Rule 4(1)(g) | No loan or statutory dues default | No default on preference dividends, term loans from banks or financial institutions, employee statutory dues, or IEPF credits; a default bars the issue for five years after it is made good. |

| Rule 4(1)(h) | No recent regulatory penalty | The company has not been penalised by a Court or Tribunal in the last three years for an offence under the RBI Act, SEBI Act, SCRA, FEMA, or any other sectoral regulator law. |

Profit Track is no longer required

Until 2019, a company could issue DVR shares only if it had a consistent track record of distributable profits for the previous three years, and the cap was 26% of post-issue paid-up equity share capital. The Companies (Share Capital and Debentures) Amendment Rules, 2019 (G.S.R. 574(E) dated 16 August 2019) removed the profit-history requirement entirely and replaced the 26% capital ceiling with the present 74% of total voting power.

Private Companies: Flexible

Private companies sit largely outside this framework. Because a private company is a closed, consent-based vehicle, the law lets its founders write their own voting architecture into the charter rather than follow the public-company template. That freedom is real, but it is conditional on the AOA actually providing for it.

MCA Notification G.S.R. 464(E) dated 5 June 2015, provides that Sections 43 and 47 of the Companies Act, 2013 do not apply to a private company where its memorandum or articles so provide. Because Rule 4 depends on Section 43, a private company that has included this exemption in its memorandum and articles is not bound by the 74% cap or the other Rule 4 conditions, and can design its own share classes and voting ratios.

What is required?

- Clear drafting in the articles

- Memorandum alignment

- Shareholder approval

- Consistency with any shareholders’ agreement

- Minority protection.

Listed & IPO-Bound Companies

Upon listing, SEBI imposes a stricter framework for superior voting rights (SR) shares to protect public shareholders. Targeted at technology founders seeking to maintain control during an IPO, this route is more restrictive than Rule 4.

Key conditions under the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 include:

- Eligible Holders: Limited to founders or promoters in executive roles.

- Special Resolution: Mandatory shareholder approval required.

- Voting Ratio: Rights must range between 2:1 and 10:1 against ordinary shares.

- Sunset Clause: Shares convert after five years

- Coattail Provisions: Superior rights lapse for resolutions affecting minority interests.

- Net-worth Limit: The holder’s individual net worth (excluding the issuer holding) cannot exceed ₹1,000 crore.

The Three Routes Compared

The same instrument behaves very differently depending on the company that issues it. A private company has the widest latitude, a public company works inside Rule 4, and a listed company answers to SEBI as well. The table below lines up the three routes against the questions founders actually ask, how high the votes can go, what cap applies, and what approval the issue needs, so the right structure for a given company is easy to read off at a glance.

| Company type | Governing framework | Aggregate voting cap | Per-share ratio limit | Approval route | Key safeguard |

|---|---|---|---|---|---|

| Private company | Sections 43 & 47 disapplied by the charter (G.S.R. 464(E), 5 June 2015) | Set by the articles; not statutorily fixed | Set by the articles; none prescribed | Members’ approval per the articles | Minority remedies (Sections 241–242); SHA discipline |

| Public / unlisted company | Section 43 + Rule 4, Companies (SC&D) Rules, 2014 | DVR voting power ≤ 74% of total voting power | None prescribed per share | Ordinary resolution + articles authority | No specified defaults; no recent regulatory penalty |

| Listed / IPO-bound company | SEBI (ICDR) Regulations, 2018 (SR framework) | SR voting subject to coattail + sunset | 2:1 minimum to 10:1 maximum | Special resolution; SR to promoters/founders | Sunset (5 + 5 years); coattail provisions |

Frequently Asked Questions

What are DVR shares under the Companies Act, 2013?

Differential voting rights shares are equity shares that carry rights different from ordinary equity — typically more dividend with fewer votes, or more votes with a smaller economic stake. Section 43 of the Companies Act, 2013 expressly allows a company limited by shares to issue equity shares with differential rights as to dividend, voting or otherwise, in line with the prescribed rules. They let founders raise capital while limiting the dilution of control, which is why promoters and family-run businesses use them. They remain equity shares throughout — the holder is a shareholder, not a lender, and shares in both profit and risk like any other equity owner.

Can one DVR share carry 10,000 votes?

For an unlisted company, the law does not set a maximum votes-per-share ratio, so an extreme ratio is not expressly forbidden. What Rule 4(1)(c) of the Companies (Share Capital and Debentures) Rules, 2014 caps is the aggregate: the combined voting power of all DVR shares cannot exceed 74% of the company’s total voting power. So a very high ratio is only workable if the total DVR voting power still stays inside that 74% ceiling, the articles authorise it, members approve it, and the structure is properly disclosed and justified. For a listed company, SEBI is far stricter and limits the superior-voting ratio to a maximum of 10:1.

What is the 74% voting-power cap on DVR shares?

Under Rule 4(1)(c) of the Companies (Share Capital and Debentures) Rules, 2014, the voting power attached to all DVR shares of a company, taken together, must not exceed 74% of the total voting power — counting every DVR share issued at any point of time. The cap is on voting power, not on the number or value of shares, which is the change the 2019 amendment introduced. In practice it means ordinary shareholders always retain at least about a quarter of the company’s votes, so DVR shares can concentrate control but cannot extinguish the ordinary shareholders’ collective voice.

Do private companies have to follow Rule 4 for DVR shares?

Not necessarily. Through MCA Notification G.S.R. 464(E) dated 5 June 2015, Sections 43 and 47 of the Companies Act, 2013 do not apply to a private company where its memorandum or articles of association so provide. Since Rule 4 hangs off Section 43, a private company that has written this carve-out into its charter is not bound by the 74% cap or the other Rule 4 conditions, and can design its own share classes and voting ratios. The freedom is conditional on the charter actually providing for it, and the company still owes its minority shareholders protection under Sections 241 and 242.

Is a three-year profit record still needed to issue DVR shares?

No — that requirement was removed in 2019. Earlier, Rule 4 allowed a DVR issue only if the company had a consistent track record of distributable profits for the previous three years. The Companies (Share Capital and Debentures) Amendment Rules, 2019 (G.S.R. 574(E) dated 16 August 2019) deleted that condition and, in the same notification, raised the cap from 26% of post-issue paid-up equity share capital to 74% of total voting power. A loss-making but otherwise compliant company can therefore issue DVR shares today, provided it clears the remaining Rule 4 conditions — chiefly a clean filing and payment record and no recent regulatory penalty.

How do SEBI’s rules change DVR shares for listed companies?

For a company that is listed or heading to an IPO, SEBI’s superior voting rights framework under the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 applies on top of the Companies Act. SR shares can be issued only to promoters or founders holding an executive position, must be approved by a special resolution, and carry voting rights in a ratio between 2:1 and 10:1 — never higher. They are time-limited: SR shares convert to ordinary shares on the fifth anniversary of listing, extendable once by five years, and coattail provisions force them to vote like ordinary shares on specified resolutions. This is a much tighter regime than Rule 4.

Summary: Differential voting rights (DVR) function as a strategic control mechanism under the Companies Act, 2013 and Rule 4. They allow a separation of voting power from economic ownership, subject to specific limits: a 74% aggregate voting cap for public companies, flexible charter-based arrangements for private firms, and a strict 10:1 SEBI ratio for listed entities. Reforms in 2019 simplified the process by removing profit-history requirements and expanding the voting cap, while maintaining essential safeguards for minority shareholders.

Implementing a compliant DVR structure requires precise drafting of articles, matching resolutions, and accurate filings. For expert assistance with capital restructuring or private limited company registration, founders can leverage Setindiabiz’s secretarial retainership service to ensure proper issuance of DVR shares.

In This Article

Author Bio

Meet Sanjeev Kumar, a distinguished advocate before the Supreme Court of India, High Courts, and National Tribunals. Founding Partner of Juriskps Law Offices, a premier law firm, he specializes in commercial, corporate, tax, arbitration, and IPR matters. His incisive legal insights enrich Setindiabiz’s blog with expert commentary.