ASISSE Return Filing for Companies & LLPs

Received an ASISSE notice from the National Statistics Office? It is a genuine statutory survey under the Collection of Statistics Act, 2008, due within one month. Our process experts classify your accounts correctly and file them accurately and on time.

🗹 Key Information of ASISSE Return Filing |

||

|---|---|---|

| 1 | Statutory Basis | Collection of Statistics Act, 2008 (7 of 2009), as amended; Collection of Statistics Rules, 2024 |

| 2 | Conducting Authority | National Statistics Office (NSO), MoSPI — Field Operations Division |

| 3 | Reference Period | FY 2024-25 (1 April 2024 – 31 March 2025) |

| 4 | Who must file | Companies (Companies Act 1956/2013) and LLPs (LLP Act 2008) in services, whose GSTIN is selected |

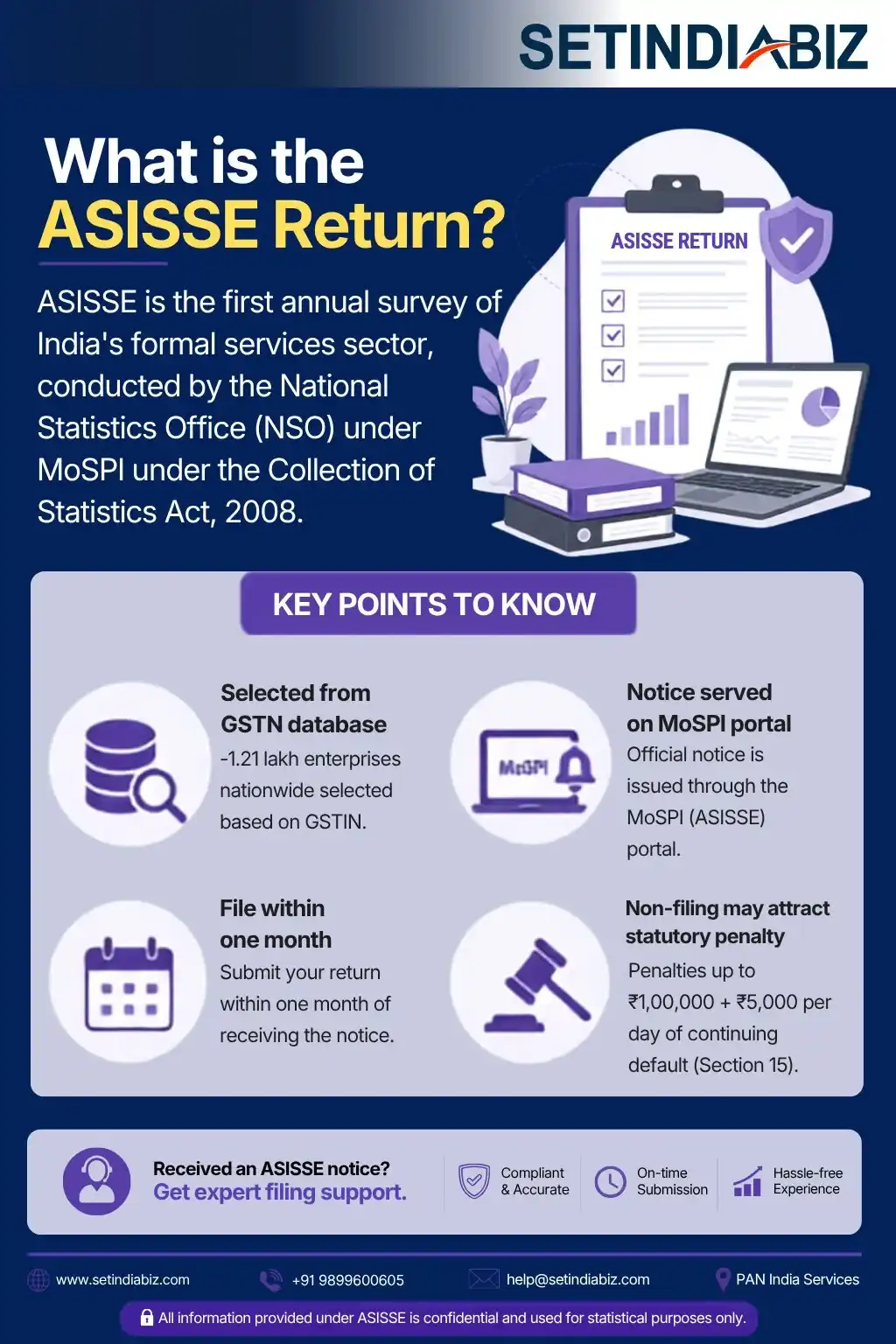

| 5 | How you were selected | Sampled from the GSTN database at the GSTIN level (~1.21 lakh enterprises nationwide) |

| 6 | Filing Deadline | Within one month of receiving the notice |

| 7 | Mode | Online, on the ASISSE web portal (mospi.gov.in) — “Balance Sheet” mode |

| 8 | Classification | NIC 2025 (activity) and CPC 3.0 (products & services) |

| 9 | Penalty for non-filing | Up to ₹1,00,000 + up to ₹5,000/day of continuing default (Section 15) |

| 10 | Confidentiality | Used only for statistics; not admissible as evidence (Sections 9 & 14) |

What is the ASISSE Return?

The Annual Survey of Incorporated Services Sector Enterprises (ASISSE) is the first-ever annual survey of India’s formal services sector, conducted by the National Statistics Office (NSO) under MoSPI as per the Collection of Statistics Act, 2008. Its reference period is FY 2024-25, and it covers companies and LLPs operating in services, including trading enterprises.

Enterprises are selected from the GSTN database and served a notice to file the return on the MoSPI web portal within one month. Setindiabiz manages the full return, reading your accounts, coding them under NIC 2025 and CPC 3.0, clearing portal validation and filing before your deadline. Contact us to get a customised quote.

Pradeep Vallat

Founder "Autonomo""Setindiabiz’s knowledgeable, disciplined, and organized team made our company registration, tax, and IPR filings smooth, hassle-free, and worry-free."

Who Has to File the ASISSE Return?

The duty to file arises under Section 6 (duty of informants) of the Collection of Statistics Act, 2008, once your enterprise’s GSTIN is drawn into the sample. ASISSE is confined to the incorporated services sector, so the obligation turns on two things: your legal form and whether your GSTIN was selected. If both conditions are met, filing is mandatory, and responsibility for compiling the return rests with the enterprise, not the NSO.

Selected Companies

Private and public limited companies in the services sector, registered under the Companies Act, 1956 or 2013.

Selected LLP

Limited Liability Partnerships (LLPs) in the services sector — registered under the LLP Act, 2008.

Selected via GSTIN

You will have received a notice with a portal link and login credentials. No notice, no filing obligation under this round.

Services & Trading

Services and trading enterprises are both covered — the notice expressly extends to trading enterprises.

Multi-GSTIN Entities.

If more than one of your GSTINs is selected, each is filed separately. never combine them.

Who is not covered

Sole proprietorships and partnership firms — they are not incorporated entities and fall outside ASISSE.

Deadline & Penalty

The ASISSE return is due within one month of receiving the notice. If needed, a written extension request must be submitted to the Statistics Officer before this deadline. Non-compliance carries significant risks: under Sections 15 and 16, companies and officers face penalties of up to ₹1,00,000, plus ₹5,000 per day for continuing defaults, with penalties adjudicated under Section 15A. Our fixed fee provides essential protection against these high statutory costs.

| No | Due Date | If you miss it (Penalty) |

|---|---|---|

| 1 | Within 1 month of receiving the notice | Penalty of up to ₹1,00,000, plus up to ₹5,000 per day of continuing default under Section 15 (as enhanced on 10 December 2024). |

| 2 | Extensions | Written request to the Statistics Officer, stating reasons |

Note: While some online articles cite a ₹5,000 penalty, the Jan Vishwas (Amendment of Provisions) Act, 2023, increased the maximum penalty to ₹1,00,000, effective 10 December 2024, and removed earlier imprisonment provisions.

⏱️ Timeline

On engagement

You share the notice and FY 2024-25 accounts; we verify the notice and selected GSTIN(s).

Scoping

We confirm the filing blocks, flag any multi-GSTIN work and share a fixed fee.

Preparation

We map and reconcile your data and code it under NIC 2025 and CPC 3.0.

Filing

We run portal validation, clear flags, submit, and share the acknowledgement.

Process of filing ASISSE Return

From the moment a notice lands to the filing of an acknowledgement, the path is short and predictable. We do the technical lifting — reading the notice, mapping your books to the schedule and clearing the portal’s checks — and keep your involvement to approving scope and supplying documents. Here is how an ASISSE filing runs with Setindiabiz.

Step 01: Share your notice

Send us the ASISSE notice and your FY 2024-25 accounts. We read the notice, confirm which GSTIN(s) are selected, the exact filing window, and that the notice is genuine.

🕒 Turnaround: Same day.

Step 02: We confirm the scope and fee

We map your obligation block by block, flag any multi-GSTIN or apportionment work, and send a fixed quote with no surprises.

🕒 Turnaround: 1 working day.

Step 03: You send documents

You share the balance sheet, P&L, payroll and asset schedules. We reconcile them against your GST returns before any portal entry.

🕒 Turnaround: 1–2 working days.

Step 04: We file and validate

Our process experts classify your data under NIC 2025 and CPC 3.0, enter it into the ASISSE portal, clear the Block 9 validation flags, and submit before the deadline.

🕒 Turnaround: 2–3 working days.

Step 05: You receive the acknowledgement

We share the portal acknowledgement for your records and will stay on for any NSO field office follow-up.

🕒 Turnaround: Immediate on filing.

Why businesses trust us

Frequently Asked Questions

ASISSE is the first-ever Annual Survey of Incorporated Services Sector Enterprises, run by the NSO under MoSPI for the reference year FY 2024-25. If your GSTIN was selected, you must file the return on the MoSPI portal under the Collection of Statistics Act, 2008.

The National Statistics Office (NSO), through the Field Operations Division of MoSPI. The legal basis is the Collection of Statistics Act, 2008 (7 of 2009) and the Collection of Statistics Rules, 2024.

Your GSTIN was drawn from the GSTN database as part of a sample of about 1.21 lakh enterprises. Selection is statistical — it is not an audit or an enquiry into your tax affairs.

Business structure, financials (balance sheet and P&L), fixed assets, working capital, employment and wages, receipts and expenses, and technology use for FY 2024-25 — captured block by block on the portal.

Yes. It is a statutory notice under the Collection of Statistics Act, 2008. Verify it against the PIB press release dated 6 April 2026 (Release ID 2249336) and confirm the portal sits on the mospi.gov.in domain.

No. ASISSE is a statistical survey only. It is not linked to any income-tax assessment, GST scrutiny or enforcement action.

No. Under Sections 9 and 14 of the Collection of Statistics Act, 2008, the information is used solely for statistics and cannot be used as evidence in any other proceeding.

Companies (Companies Act 1956/2013) and LLPs (LLP Act 2008) in the services sector whose GSTIN has been selected. Proprietorships and partnership firms are not covered.

Yes, if you are a company or an LLP and have selected your GSTIN. The survey expressly covers services-sector enterprises, including trading enterprises.

Within one month of the date you receive the notice. The deadline runs from receipt, not from a fixed calendar date.

Up to ₹1,00,000 under Section 15 of the Collection of Statistics Act, 2008, plus up to ₹5,000 for each day the default continues.

₹5,000 was the pre-amendment penalty. The Jan Vishwas (Amendment of Provisions) Act, 2023 raised it to ₹1,00,000 with effect from 10 December 2024.

An adjudicating officer under Section 15A, with an appeal to the appellate authority under Section 15B. Unpaid penalties are recoverable as arrears of land revenue.

Under Section 23 (offences by companies), officers responsible for the default can be held liable — so it is not a risk to leave unattended.

Yes. We can file on a priority basis and, where appropriate, submit a written request to the Statistics Officer explaining the delay to help limit your exposure.

The FY 2024-25 balance sheet with schedules, P&L, payroll/wage register, fixed-asset and depreciation schedule, working-capital details, your GSTIN(s) and NIC code, and the auditor’s report.

Activities are coded under NIC 2025, and products and services under CPC 3.0 (Draft) — the classifications MoSPI uses for ASISSE.

Yes. Where more than one GSTIN is selected, each is filed separately, with apportionment from your consolidated books — never a rough split.

Typically, about a week from receiving your notice and accounts, comfortably inside the one-month window. Rush filing is available.

From ₹4,999 (plus 18% GST) for a single-GSTIN, single-activity filing; ₹8,999 for multi-activity coding and validation; and a custom quote for multiple GSTINs or group entities.

No. The Government charges no fee to file the ASISSE return; our fee is purely for professional assistance.

Yes. ASISSE data is protected by Sections 9 and 14 of the Collection of Statistics Act, 2008, and we handle your accounts under strict confidentiality.

Setindiabiz is Trusted By Leading Brands