Proprietorship Formation Start Your Business in 5–7 Days

A sole proprietorship is the simplest way to start a business in India — no incorporation, no separate PAN. We bundle the Udyam and GST registrations your bank needs under the 2025 RBI KYC Directions, and walk your current account through to the first invoice.

🗹 Key Information of Sole Proprietor |

||

|---|---|---|

| 1 | Statutory Basis | No formal incorporation or registration required. Tax in the hands of the sole proprietor — under the Income-tax Act, 1961, for FY 2025–26 (returns due July/October 2026) and under the Income-tax Act, 2025 for Tax Year 2026–27 onwards. No separate PAN required. |

| 2 | Timeline | Same day for Route 1 (trade in own name). 5–7 working days for Route 2 (trade under a brand name). |

| 3 | Cost | Professional fee per package (starts at ₹2,499). Govt fee NIL |

| 4 | For Indians | Yes: any Indian citizen aged 18+ can start a proprietorship. |

| 5 | For NRI / OCI | Yes: on a non-repatriation basis |

| 6 | For Foreigners | Not permitted. |

| 7 | Liability | Unlimited (the proprietor is personally liable for all firm debts.) |

| 8 | Brand / IP protection | Optional but useful: a notarised brand-adoption affidavit or a newspaper notice fixes the date of first use under Section 34, Trade Marks Act, 1999; a trademark application gives full registered rights. |

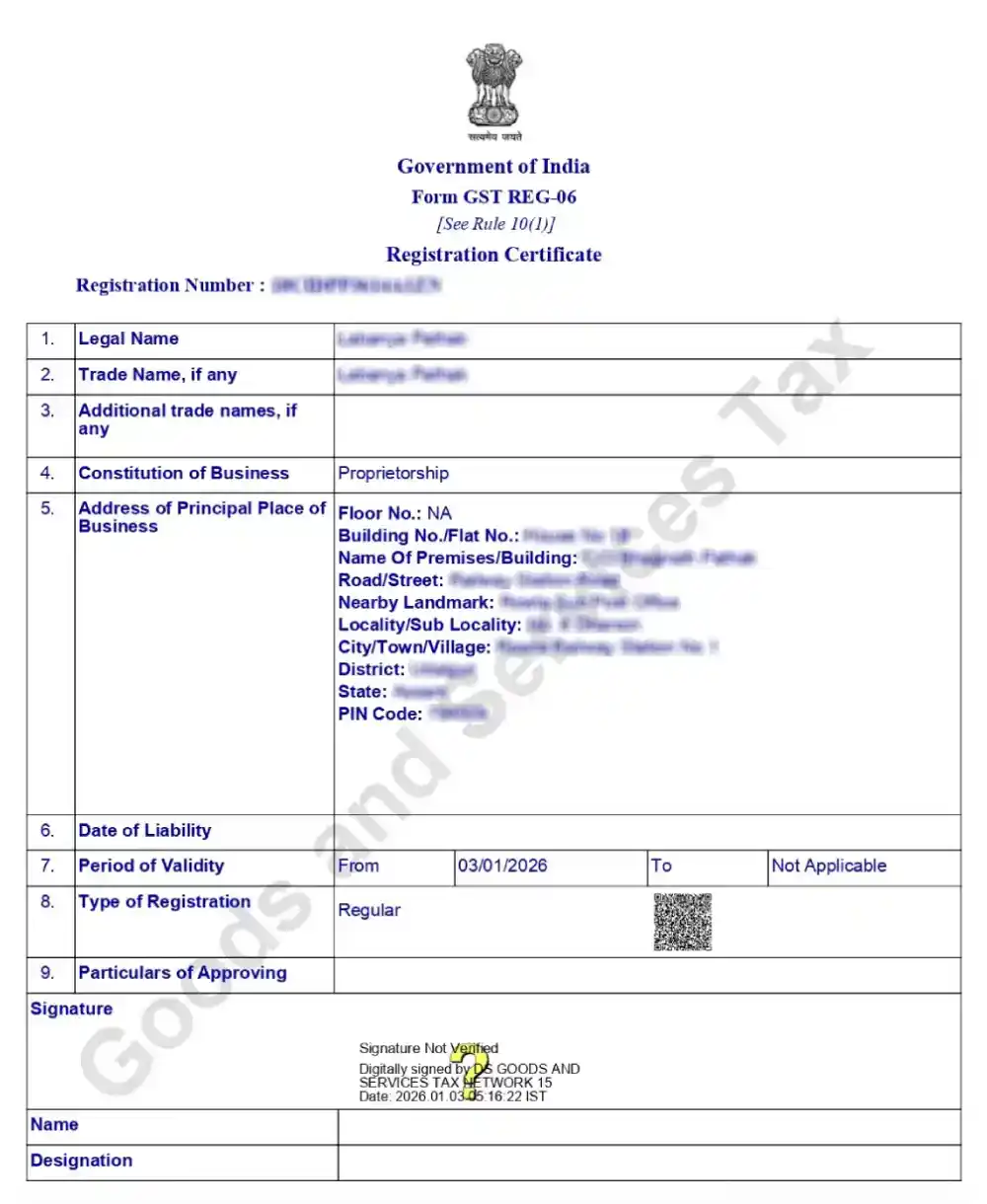

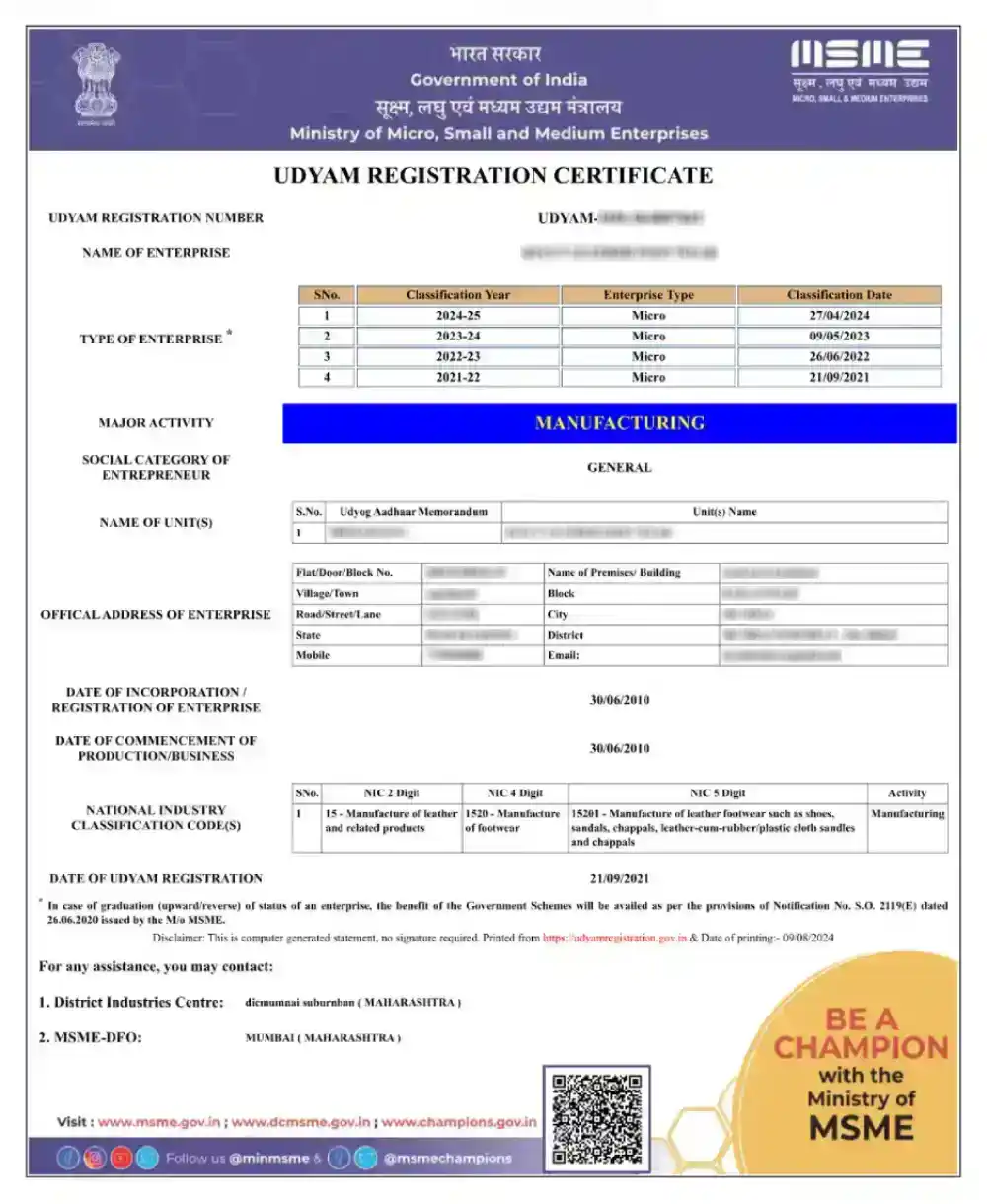

Sample of GST & MSME Registration

What is a sole proprietorship?

A sole proprietorship is owned and run by one person — the proprietor and the firm are the same legal person, there is no incorporation under any Act of Parliament, and no separate PAN. Business income is taxed in the proprietor’s hands under the Income-tax Act, 1961, for FY 2025-26 and under the Income-tax Act, 2025 from Tax Year 2026-27 onwards.

The firm itself needs no central registration. What you need are activity-specific registrations — typically Udyam under the MSMED Act, 2006, GST under the CGST Act, 2017, and a State Shops & Establishment licence — so the bank can open a current account in the firm’s name under the 2025 RBI KYC Directions. Our process experts complete the bundle in 5–7 working days.

Pradeep Vallat

Founder "Autonomo""Setindiabiz’s knowledgeable, disciplined, and organized team made our company registration, tax, and IPR filings smooth, hassle-free, and worry-free."

Two Routes to Set Up Your Proprietorship

A sole proprietorship can be set up in one of two ways, and the route you pick shapes the entire downstream bundle, what registrations you actually need, what your bank will ask for, and whether a brand-adoption affidavit is worth filing. Either way, the proprietorship itself requires no incorporation; the activity-specific registrations simply ensure that banking, invoicing, and compliance run cleanly from day one. Decide the route before we file anything.

🧭 Route 1: Trade in your own name

Trading in your own name involves no separate brand, removing the need for trademark protection. Current account opening is simpler as banks typically don’t require two firm-name documents. MSME and GST registrations are optional unless legally mandated by your turnover or specific activities like e-commerce or inter-state sales.

- Easiest to Start

- There is no brand to protect

- MSME or GST are optional

- Paperwork (Optional)

Best for: professionals, consultants, freelancers, and small traders billing under their own name with no plan to build a separate brand.

🧭 Route 2: Trade under a brand name

Trading under a brand name requires no mandatory registration, but banks need two RBI-notified documents to open a current account. MSME (Udyam) and GST registrations are the easiest pair to provide. Additionally, recording your brand’s adoption date via affidavit or notice helps secure future trademark protection.

- Brand’s adoption date affidavit

- Brand’s adoption date Public Notice

- MSME (Udyam) Registration

- GST registrations

Best for: founders building a consumer-facing or B2B brand, eCommerce sellers, D2C operators, and anyone who wants the firm name on invoices, signboards, and marketing.

Brand-adoption affidavit (recommended): To lock in the date on which you first adopted the brand (Trademark), which becomes your “prior use” date if anyone later challenges you under Section 34 of the Trade Marks Act, 1999, we prepare a notarised affidavit (or, alternatively, a newspaper notice). Optional, but valuable if you intend to file a trademark later or fend off a copycat.

Eligibility / Minimum Requirements

A sole proprietorship is the least-regulated business form in India, but a small set of statutory thresholds applies to capacity, residency, place of business, and lawful activity. The list below is exhaustive for a standard, non-licensed business.

Single owner only.

Only one natural person can be the proprietor — no co-owners. For two or more owners, choose a partnership or LLP.

Indian citizen aged 18+.

The proprietor must be an Indian citizen of majority age, capable of entering into a lawful contract under Section 11 of the Indian Contract Act, 1872.

NRI / OCI with conditions.

NRIs and OCIs may run a sole proprietorship in India only on a non-repatriation basis, under Schedule 4 of the FEM (Non-Debt Instruments) Rules, 2019.

Registered place of business.

Even though no entity registration is required, every proprietorship must declare a Principal Place of Business with proof of valid premises.

A lawful activity

The business must be legal; food, drug, or financial activities require a specific licence (FSSAI, Drug Licence, NBFC registration, etc.) before you begin operations.

No minimum capital.

No statutory floor in the capital. Introduce or withdraw funds at your discretion as proprietor's drawings.

Pricing for the Establishment of a Sole Proprietorship |

Basic ₹2499 |

Silver ₹7499 |

||

|---|---|---|---|---|

| No. | Best Suited for | Solo founders need a current account. | Active firms with ongoing GST Returns. | Brand needing prior-use defence. |

| 1 | Expert Consultation 30-minute strategy call with a Setindiabiz process expert to confirm your route, applicable registrations, and bank-account plan before we start the bundle. | ✔ | ✔ | ✔ |

| 2 | GST Registration (U/rule 14A) Simplified GST registration under Rule 14A of the CGST Rules, 2017 — for small taxpayers with monthly B2B output tax up to ₹2.5 lakh; 3-day Aadhaar-authenticated approval. | ✔ | ✔ | ✔ |

| 3 | MSME Registration Udyam Registration under the MSMED Act, 2006, filed via Aadhaar OTP. Free, instantly issued, and the easiest activity proof to satisfy Paragraph 31 of the RBI (Commercial Banks – KYC) Directions, 2025. | ✔ | ✔ | ✔ |

| 4 | Dedicated Relationship Manager A named single point of contact who tracks your full bundle end-to-end, coordinates with the bank, and stays on call for all queries during your 5–7-day setup window. | ✘ | ✔ | ✔ |

| 5 | GST Return for Six Months Six months of GST return filings — covering outward supplies and tax payment — whether your firm files monthly returns or under the quarterly QRMP scheme. | ✘ | ✔ | ✔ |

| 6 | TAN Number Allotment Tax Deduction Account Number under Section 203A of the Income-tax Act, 1961, continuing under the Income-tax Act, 2025 — required once you deduct TDS on salaries, rent, or vendor payments above the threshold. | ✘ | ✔ | ✔ |

| 7 | Shops Act Registration State-level registration with the Labour Department under the relevant State Shops and Establishment Act — mandatory for non-manufacturing premises with one or more employees. | ✘ | ✔ | ✔ |

| 8 | Brand Name Availability Search Pre-adoption search on the IP India trademark register and the MCA portal to flag conflicts before you commit to a brand name — avoids later Section 11 oppositions and rebrand costs. | ✘ | ✘ | ✔ |

| 9 | Drafting of Brand Adoption Affidavit Notarised affidavit on ₹100 stamp paper recording the date of first use of your brand — anchors any later prior-use claim under Section 34 of the Trade Marks Act, 1999. | ✘ | ✘ | ✔ |

| 10 | Drafting of Newspaper Notice A formal public notice drafted in the firm's name, declaring brand adoption and the date of first use, establishes constructive public notice of your prior-use claim. | ✘ | ✘ | ✔ |

| 11 | Arranging Newspaper Advertisement Coordinating publication of the brand-adoption notice in one English and one regional vernacular daily newspaper publication charges are on actuals, paid directly by you. | ✘ | ✘ | ✔ |

|

Calculate Cost & Place Order

All-inclusive pricing. No hidden charges.

→

|

||||

- Our packages include GST filing via the Rule 14A scheme for taxpayers with a monthly B2B tax liability under ₹2.5 lakh. Custom quotes are required for scenarios involving high turnover, e-commerce, casual, or non-resident status. Contact us for expert scoping.

- All government fees, stamp duty on the brand affidavit, and any state-specific Shops & Estb. Fees are charged on actuals. Newspaper advertisement publication charges are on actuals, paid directly by you. GST on the professional fee is extra. Setindiabiz is a private professional services firm and is not affiliated with any government body. We do not issue government documents.

Timeline for Proprietorship Registration

KYC & Route Choice

We collect your KYC, confirm whether you trade in your own name or under a brand, and lock the bundle.

Udyam / MSME

We file Udyam on udyamregistration.gov.in (Aadhaar OTP); the certificate is generated instantly. For Route 2, we lodge the brand-adoption affidavit.

GST Registration

We file REG-01 on the GST portal with Aadhaar e-KYC under Rule 8(4A); GSTIN within 3 working days under Rule 14A.

Current Account

Bank verifies under Paragraph 31, Chapter VI(B), RBI (Commercial Banks – KYC) Directions, 2025; account opens; first invoice goes out.

Stepwise Process to Set Up a Sole Proprietorship

Seven structured steps, calibrated to Route 2 (brand name), which carries the full bundle. Route 1 (own name) collapses Steps 2, 4 and 5 where no separate registration is independently required by your activity or turnover. The end-state is the same in both routes: KYC in order, registrations issued, a current account open, first invoice raised under the firm’s name. The whole sequence runs end-to-end in 5–7 working days.

Step 01: Collect KYC and confirm the business name

First, we collect your PAN, Aadhaar and recent address proof, and confirm whether you will trade in your own name or under a brand. This one choice decides which registrations you actually need, so we settle it before filing anything.

⏳ Turnaround: Same day, on receipt of documents

Step 02: Adopt and declare your brand name

For Route 2, we run a trademark search on the IP India portal and confirm the brand is free to adopt. We then prepare a notarised affidavit recording the date of first use — useful for any later prior-use claim under Section 34 of the Trade Marks Act, 1999.

⏳ Turnaround: 1 working day; affidavit notarised the same day.

Step 03: Register on the Udyam (MSME) portal

Next, we file your Udyam Registration on udyamregistration.gov.in using your Aadhaar and PAN, an OTP-based self-declaration under the MSMED Act, 2006. Udyam is free, takes minutes, and gives you a certificate in the firm’s name. The certificate counts as an activity proof under Paragraph 31 of the RBI (Commercial Banks – KYC) Directions, 2025.

⏳ Turnaround: Same day; Udyam certificate generated instantly.

Step 04: Apply for GST registration where it is required

If your business needs it, we file your GST registration under the CGST Act, 2017. GST is compulsory once turnover crosses ₹40 lakh for goods or ₹20 lakh for services (lower in special-category states), and from day one for inter-state or e-commerce supply. We file REG-01 with Aadhaar e-KYC under Rule 8(4A) and obtain your GSTIN within 3 working days under the Rule 14A simplified scheme.

⏳ Turnaround: 3 working days under Rule 14A.

Step 05: Obtain Shops and Establishment registration

Where your state requires it, we obtain your Shops and Establishments registration. This licence proves your place of business and, in many states, is itself accepted as a valid document for opening the current account.

⏳ Turnaround: Varies by state; typically 2–7 days.

Step 06: Open your current account and start operating

With your certificates ready, we help you open a current account in the firm’s name. For a brand-name firm, the bank needs any two documents from the RBI list, usually your Udyam and GST certificates. The bank branch verifies under Paragraph 31 of Chapter VI(B) of the RBI (Commercial Banks – KYC) Directions, 2025. Once the bank account is opened, you can issue an invoice in the firm’s name.

⏳ Turnaround: Bank-dependent — typically 2–4 working days from submission.

Step 07: Add any industry-specific licences you need

Finally, we add any licence your activity needs, such as FSSAI Registration for food business, IEC for imports and exports, a drug or trade licence — so you operate fully within the law from day one.

⏳ Turnaround: Depends on the licence; we advise upfront

Why businesses trust us

Documents Required to Open a Sole Proprietorship Bank Account

Every bank in India follows the RBI (Commercial Banks – Know Your Customer) Directions, 2025 (RBI/DOR/2025-26/169 dated 28 November 2025, amended 29 December 2025 by RBI/2025-26/166), which replaced the 2016 KYC Master Direction. To open a current account in the firm’s brand name, the bank needs any two documents in the firm’s name as proof of business or activity under Paragraph 31 of Chapter VI(B). The RBI’s list does not split into separate identity and address proofs — that is a bank-form convention; most listed documents serve as both. Utility bills are address-only.

Identity Proof of the Firm

- Udyam Registration Certificate

- GST Registration (Form REG-06)

- Municipal Shop & Establishment License

- DGFT-issued IEC Code

- Professional Practice Certificate (ICAI, BCI)

- Tax Registrations (Sales, Service,

- Professional Tax Registration

- Legacy CST/VAT Certificates

- Income and Sales Tax Returns

- Proprietor’s ITR reflecting firm income

Address Proof of the Firm

- Udyam Registration Certificate

- GST Registration (Form REG-06)

- Municipal Shop & Establishment Licence

- Import Export Code (IEC) from DGFT

- Professional Practice Certificate in firm name

- Sales, Service, or Professional Tax registration

- Legacy CST / VAT certificates

- Sales and Income Tax returns

- The proprietor’s ITR showing business income

- Utility bills (Electricity, Water, Landline)

Sole Proprietorship vs One Person Company (OPC)

A sole proprietorship and a One Person Company both let one founder run the business alone — but they sit on opposite ends of the cost/protection trade-off. A proprietorship is fast, cheap and informal; an OPC carries the corporate structure with limited liability but requires ROC filings every year. The table below compares them across nine attributes that actually matter at the point of decision formation, liability, compliance, tax and conversion — so you can pick on the facts.

| No | Particulars | Sole Proprietorship | One Person Company (OPC) |

|---|---|---|---|

| 1 | Governing law | No incorporation statute; activity-specific Acts apply | Section 2(62) + Section 3(1)(c) of the Companies Act, 2013 |

| 2 | Separate legal identity | No — proprietor and firm are the same | Yes — distinct legal person, separate from the member |

| 3 | Liability | Unlimited; personal assets at risk | Limited to subscribed capital |

| 4 | Setup time | Same day to 5–7 working days | 7–15 working days |

| 5 | Incorporation cost | Govt fee on actuals; professional fee separate | Higher: INC-32 SPICe+ filing fee + stamp duty + DSC |

| 6 | Annual compliance | ITR only (with tax audit if turnover crosses the prescribed threshold under the Income-tax Act) | ROC filings (AOC-4, MGT-7A), board meeting, ITR |

| 7 | FDI / Foreign investment | Not permitted (except NRI/OCI on non-repatriation) | Not permitted under Schedule 1, FEM (NDI) Rules, 2019 |

| 8 | Conversion option | Convertible to Pvt Ltd or LLP later | Convertible to Pvt Ltd if turnover/PUC thresholds crossed |

| 9 | Best for | Solo professionals, traders, freelancers | Solo founders wanting limited liability + corporate identity |

| For a deeper comparison, see our one-person company registration page. | |||

Tax Rate of sole Proprietorship

A sole proprietorship is not a separate taxpayer; its income is added to the proprietor’s personal income and taxed at individual slab rates. The slabs below are for a resident individual below 60 years. The new tax regime (Section 115BAC) is the default; the old regime stays available as an option. Budget 2026 left the slabs unchanged, so FY 2025-26 (taxed under the Income-tax Act, 1961) and FY 2026-27 (under the Income-tax Act, 2025) carry the same rates.

New tax regime (default) — resident individual below 60

| No | Income slab | FY 2025-26 (AY 2026-27) | FY 2026-27 (AY 2027-28) |

|---|---|---|---|

| 1 | Up to ₹4,00,000 | Nil | Nil |

| 2 | ₹4,00,001 – ₹8,00,000 | 5%mall taxpayers can opt for Rule 14A simplified registration. | 5% |

| 3 | ₹8,00,001 – ₹12,00,000 | 10% | 10% |

| 4 | ₹12,00,001 – ₹16,00,000 | 15% | 15% |

| 5 | ₹16,00,001 – ₹20,00,000 | 20% | 20% |

| 6 | ₹20,00,001 – ₹24,00,000 | 25% | 25% |

| 7 | Above ₹24,00,000 | 30% | 30% |

Old tax regime (optional) — resident individual below 60

| No | Income slab | FY 2025-26 (AY 2026-27) | FY 2026-27 (AY 2027-28) |

|---|---|---|---|

| 1 | Up to ₹2,50,000 | Nil | Nil |

| 2 | ₹2,50,001 – ₹5,00,000 | 5% | 5% |

| 3 | ₹5,00,001 – ₹10,00,000 | 20% | 20% |

| 4 | Above ₹10,00,000 | 30% | 30% |

On top of the slab tax, a 4% health and education cess applies in both years, and a surcharge applies at higher incomes (from 10% above ₹50 lakh, capped at 25% under the new regime). Under the new regime, a Section 87A rebate makes taxable income up to ₹12,00,000 effectively tax-free; under the old regime, the rebate covers income up to ₹5,00,000. The old regime gave a higher basic exemption to senior citizens (60–80: ₹3,00,000) and super-senior citizens (80+: ₹5,00,000); those are not shown here, as this table assumes a proprietor below 60.

Frequently Asked Questions

A sole proprietorship is a business owned and run by one person, with no separation between the owner and the firm. It is not a separate legal entity and needs no incorporation under any Act. The proprietor uses their own PAN, keeps all profits, and bears unlimited liability for the firm’s debts.

No. A sole proprietorship has no legal identity apart from its owner. The proprietor and the business are one and the same in law, which is why the proprietor’s PAN is used, and the proprietor is personally liable for all business obligations.

No single registration is legally mandatory to start a proprietorship. You register only what your business needs — GST if you cross the threshold or fall within the Section 24 compulsory triggers, MSME (Udyam) for benefits and banking, or a Shops & Establishment licence where your state requires it.

A proprietorship has a single owner and no separate legal status, while a partnership firm has two or more partners under the Indian Partnership Act, 1932. Both carry unlimited liability, but a partnership is governed by a partnership deed that sets out profit-sharing and roles.

A sole proprietorship has no separate legal identity and unlimited liability; an OPC is incorporated under Section 3(1)(c) of the Companies Act, 2013, has a separate legal identity, and limits liability to subscribed capital. OPC has higher setup and compliance costs and is suited to founders who want corporate protection from day one.

Route 1: trade in your own name — no brand, no separate registrations needed unless your business independently requires them. Route 2: trade under a brand name — needs two activity proofs in the firm’s name under Paragraph 31 of the 2025 RBI KYC Directions to open a current account. The two cheapest are Udyam and GST.

Yes. You may trade under a brand or trade name different from your own. No registration is compulsory just to use a brand name, but to open a current account in that name, the bank needs any two documents in the firm’s name under Paragraph 31 of the 2025 RBI KYC Direction.

No, a trademark is not required to start. If you trade in your own name, there is no brand to protect. If you adopt a brand name and want exclusive rights to it, a trademark under the Trade Marks Act, 1999, is advisable but optional.

Record it through a notarised affidavit (on ₹100 stamp paper) or a newspaper notice declaring the date you began using the brand. This fixes your first-use date — the basis of any later prior-use defence under Section 34 of the Trade Marks Act, 1999.

Any Indian citizen aged 18+ with a valid PAN and Aadhaar can start one — only one owner is permitted. NRIs and OCIs may also run a proprietorship in India, but only on a non-repatriation basis under Schedule 4 of the FEM (Non-Debt Instruments) Rules, 2019. Foreign nationals generally cannot.

No. A sole proprietorship can have only one owner. If two or more people want to run a business together, they should form a partnership firm under the Indian Partnership Act, 1932 or an LLP under the LLP Act, 2008 instead.

There is no statutory minimum capital under any Act for a sole proprietorship — unlike the historical position for incorporated entities. You introduce or withdraw funds at your discretion as the proprietor’s drawings, depending on what your business needs.

No. A sole proprietorship does not have its own PAN because it is not a separate legal entity. All business income, registrations, and tax filings are processed under the proprietor’s individual PAN, which is also used for GST and the firm’s current account.

Only if it applies to you. GST registration is mandatory once turnover crosses ₹40 lakh for goods or ₹20 lakh for services (lower in special-category states), and from the first transaction under Section 24 triggers — inter-state supply, e-commerce sale, or reverse charge. Small taxpayers can opt for Rule 14A simplified registration.

It is optional but useful. Udyam registration under the MSMED Act, 2006, is free, provides a certificate in the firm’s name accepted by banks, and unlocks government benefits, subsidies, and easier credit. Many proprietors take it first for exactly these reasons.

It is a state-level licence regulating commercial establishments, obtained under the relevant State Shops and Establishments Act. Many proprietors take it to prove their place of business; in several states, it is also accepted as a valid document for opening a current account.

The bank follows the RBI (Commercial Banks – KYC) Directions, 2025. For a brand-name firm, it needs any two documents in the firm’s name from the Paragraph 31 list — commonly the Udyam certificate, GST certificate, Shops & Establishment licence, or a utility bill. Trading in your own name needs lighter documentation.

Under Paragraph 31 of Chapter VI(B) of the RBI (Commercial Banks – KYC) Directions, 2025, banks must collect two documents in the firm’s name as proof of business or activity before opening a current account in the proprietorship’s brand name. Where two proofs are impossible to procure, Paragraph 32 permits one proof plus a contact-point verification.

Rule 14A of the CGST Rules, 2017, is a simplified scheme, effective 1 November 2025, under Notification No. 18/2025. It lets small taxpayers with a monthly B2B output tax of up to ₹2.5 lakh obtain a GSTIN within 3 working days via Aadhaar OTP. Our packages cover this scheme; larger cases are scoped on a custom quote basis.

Yes. The 2016 KYC Master Direction was repealed on 28 November 2025 and replaced by the RBI (Commercial Banks – KYC) Directions, 2025. The two-document rule for opening a proprietorship current account is now in Paragraph 31 of Chapter VI(B). The list of acceptable documents is substantively unchanged from the 2016 version.

Typically, 5–7 working days end-to-end — 1 day for documentation and Udyam, 3 working days for GST under Rule 14A, and 1–3 days for the current account. Timelines may vary with GST officer review and state-level processing for the Shops & Establishment licence.

Udyam and GST registration carry no government fee. Stamp duty on the brand-adoption affidavit is ₹50–₹100, depending on the state. Shops & Establishment fee varies by State — typically ₹100–₹3,000. Industry-specific licences carry their own fees, charged at actuals. Our professional fee is quoted upfront.

Business income is added to the proprietor’s personal income and taxed at slab rates — under the Income-tax Act, 1961, for FY 2025–26 (returns due July/October 2026), and under the Income-tax Act, 2025, for Tax Year 2026–27 onwards. There is no separate company tax. Tax audit applies once turnover crosses ₹1 crore (or ₹10 crore if cash transactions stay under 5%).

Yes. A proprietorship can be converted into an OPC, Private Limited Company, or LLP as it grows — by incorporating the new entity and transferring the business under a Business Transfer Agreement. Subject to prescribed conditions, the conversion may qualify for capital-gains exemption under Section 47(xiv) of the Income-tax Act, 1961 (and its corresponding provision under the Income-tax Act, 2025).

Setindiabiz is Trusted By Leading Brands