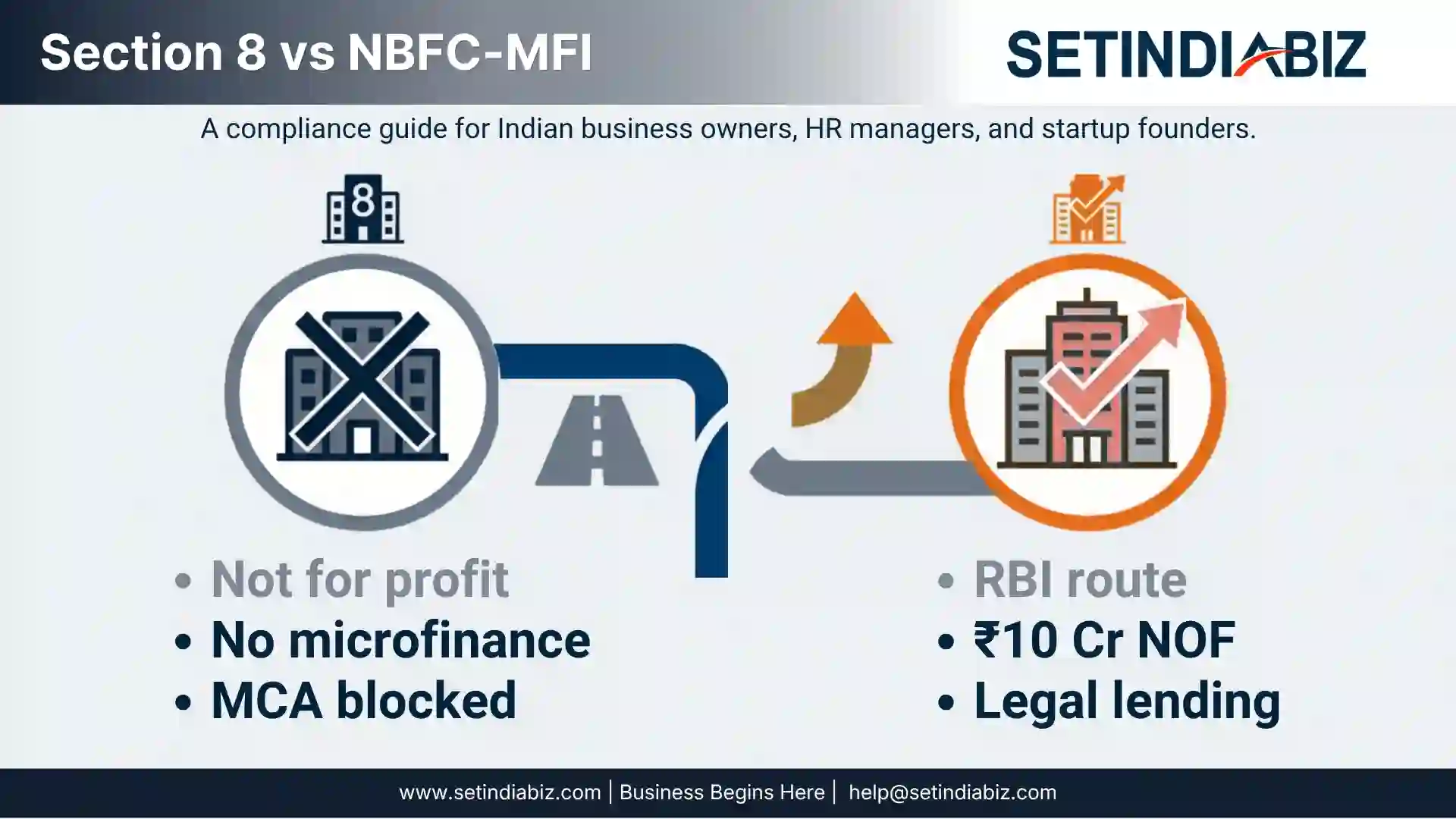

Aspiring entrepreneurs frequently ask if a Section 8 company can be registered for a microfinance business. The answer is a clear No. The Ministry of Corporate Affairs (MCA) strictly prohibits the use or amendment of a Section 8 company for micro-finance activities. The only legal way to enter the microfinance sector is to register as an NBFC-MFI (Non-Banking Financial Company – Micro Finance Institution) with approval from the Reserve Bank of India (RBI). This guide will detail the reasons for the prohibition, the relevant MCA/RBI regulations, and the complete process for legally starting a microfinance business in India.

What is a Section 8 Company?

A Section 8 company is a type of company registered under Section 8 of the Companies Act, 2013, for promoting charitable objectives such as commerce, art, science, education, sports, social welfare, religion, charity, or environmental protection. These companies operate on a not-for-profit basis and are prohibited from distributing dividends to their members. Any profits earned must be applied towards promoting the company’s objects.

Section 8 companies enjoy privileges such as exemption from using “Limited” or “Private Limited” in their name and can be incorporated with lower capital than other company forms. Due to these benefits, many entrepreneurs tried to use the Section 8 structure as a shortcut to enter microfinance, a practice the MCA has now stopped.

Why Section 8 Companies Cannot Do Micro Finance Business

The Core Issue: In India, the Reserve Bank of India (RBI) regulates lending and financial services under the RBI Act, 1934. Only registered Non-Banking Financial Companies (NBFCs) with an RBI Certificate of Registration (CoR) are authorised to conduct financial business, including microfinance. Although a prior RBI Master Circular (July 1, 2015) exempted Section 8 companies from certain micro-lending limits, the Ministry of Corporate Affairs noted widespread misuse. Many Section 8 companies engaged in microfinance without meeting the mandated Net Owned Fund (NOF) and other RBI regulatory requirements.

MCA’s Prohibition (A Timeline of Circulars): The MCA issued a series of directions and circulars to stop this misuse. Here is the chronological timeline of how this prohibition evolved:

| Date | Document | Key Direction |

|---|---|---|

| 10 February 2020 | MCA Direction Letter No. 05/33/2017-CL.V | Directed CRC (Central Registration Centre) not to allow incorporation of Section 8 companies with micro finance objects, as they do not comply with the NOF criterion laid down by RBI’s Non-Banking Financial Company – Micro Finance Institutions (Reserve Bank) Directions, 2011. |

| 31 August 2020 | MCA Letter (File No. 05/33/2017-CL-V) to All ROCs and RDs | Reiterated the direction and noted that companies were being incorporated without micro finance objects, but were later amending their MOA to include micro finance/micro credit activities. Directed ROCs not to allow such alterations unless NOF and other RBI requirements were complied with. |

| 30 May 2022 | General Circular No. 05/2022 (File No. Policy-02/02/2022-CL-MCA) | The most comprehensive direction — observed that Section 8 companies were passing Special Resolutions, changing Activity Codes, and filing e-form MGT-14 to alter their objects for micro finance. Directed immediate action by ROCs to prevent this. Also directed DGCoA to ensure strict compliance across all ROCs. |

What General Circular No. 05/2022 Says

The General Circular No. 05/2022 dated 30 May 2022 is the definitive MCA direction on this matter. The key observations and directions in this circular are as follows:

It was observed that various Section 8 companies altered their object clauses to carry out microfinance activities by passing Special Resolutions, changing Activity Codes, and filing e-form MGT-14 with ROCs. The MCA noted that although ROC (CRC) did not allow incorporation with microfinance objects initially, companies found workarounds through post-incorporation amendments.

The Only Legal Route – NBFC-MFI Registration with RBI

To start a microfinance business in India legally, you must register as an NBFC-MFI with the Reserve Bank of India. This is governed by the RBI Master Direction – Reserve Bank of India (Regulatory Framework for Microfinance Loans) Directions, 2022 (RBI/DOR/2021-22/89, dated March 14, 2022, updated July 17, 2025).

What is an NBFC-MFI?

An NBFC-MFI is a non-deposit-taking NBFC with at least 60% of its total assets (net of intangible assets) deployed towards “microfinance loans” as defined by RBI’s Regulatory Framework for Microfinance Loans, 2022. This threshold was revised from 75% to 60% by RBI Circular No. RBI/2025-26/44 dated June 6, 2025, to provide operational flexibility while keeping focus on the core microfinance mandate.

What is a Microfinance Loan?

Under the RBI’s framework, a microfinance loan is a collateral-free loan to a household with an annual income of up to ₹3,00,000. A household means an individual family unit—husband, wife, and their unmarried children.

Eligibility to Start a Micro Finance Business (NBFC-MFI)

| No | Requirement | Details |

|---|---|---|

| 1 | Entity Type | Must be a company registered under the Companies Act, 2013 (or earlier Companies Act, 1956) |

| 2 | Net Owned Fund (NOF) | Minimum ₹10 crore (as per RBI’s Scale-Based Regulation Framework, October 2021). The glide path deadline for existing NBFCs to achieve ₹10 crore NOF is March 31, 2027. |

| 3 | Qualifying Assets | At least 60% of total assets (net of intangible assets) must be microfinance loans (revised from 75% vide RBI Circular dated June 6, 2025) |

| 4 | Board Experience | At least one director must have relevant experience of having worked in a bank or NBFC |

| 5 | Business Plan | A detailed 5-year business plan covering objectives, market analysis, financial projections, HR plan, and risk management |

| 6 | Capital Adequacy | Must maintain 15% CRAR (Capital to Risk-Weighted Assets Ratio), with Tier-I capital of at least 10% |

| 7 | Compliance Infrastructure | Must have robust KYC/AML systems, Fair Practice Code, grievance redressal mechanism, and reporting systems to Credit Information Companies |

NOF Glide Path for Existing NBFCs

RBI provided a phased glide path for existing NBFCs to meet enhanced NOF requirements under the Scale-Based Regulation (SBR) Framework:

| NBFC Type | Earlier NOF | By March 31, 2025 | By March 31, 2027 |

| NBFC-ICC | ₹2 crore | ₹5 crore | ₹10 crore |

| NBFC-MFI | ₹5 crore (₹2 crore in NE Region) | ₹7 crore (₹5 crore in NE Region) | ₹10 crore |

| NBFC-Factors | ₹5 crore | ₹7 crore | ₹10 crore |

Note: As per the latest RBI clarification, there shall be no distinction in the NOF requirement for NBFCs registered in the North East Region for the final target of ₹10 crore.

Step-by-Step Process to Register an NBFC-MFI 📝

Registering an NBFC-MFI involves two major stages: company incorporation under the Companies Act and obtaining the Certificate of Registration (CoR) from the RBI. Here is the step-by-step process:

Step 1: Incorporate a Company Under the Companies Act, 2013.

Register a public or private limited company with the Registrar of Companies (ROC) via the SPICe+ form. The Memorandum of Association (MOA) should include financial services and microfinance lending objects. Obtain the Certificate of Incorporation (CoI) and arrange minimum paid-up capital equal to the NOF requirement.

Step 2: Arrange Net Owned Fund (NOF) of ₹10 Crore.

The company must have an NOF of at least ₹10 crore in equity capital and free reserves, less accumulated losses, deferred revenue expenditure, and intangible assets. Obtain a Chartered Accountant’s certificate confirming the NOF.

Step 3: Prepare a Comprehensive Business Plan.

Draft a detailed 5-year business plan covering the company’s objectives, target market, geographic areas of operation, loan products, financial projections, risk management strategy, HR plan, and technology infrastructure for microfinance operations.

Step 4: Submit Online Application to RBI

Apply online through the RBI’s COSMOS portal for a Certificate of Registration as an NBFC-MFI. The application must include all required documents, audited financial statements, directors’ profiles, business plan, and the CA certificate of NOF.

Step 5: Submit a hard copy to the RBI Regional Office.

After online submission, submit a physical copy of the complete application and all supporting documents to the RBI Regional Office under whose jurisdiction the company’s registered office falls.

Step 6: RBI Due Diligence and Approval.

RBI will thoroughly examine the application, including background checks of promoters and directors, assessment of the business plan, and compliance with norms. The process typically takes 6 to 12 months from application, depending on documentation completeness and RBI processing times.

Step 7: Obtain Certificate of Registration (CoR)

Upon satisfactory completion of due diligence, the RBI issues a Certificate of Registration (CoR) authorising the company to commence micro finance business as an NBFC-MFI.

Section 8 Company vs. NBFC-MFI — Key Differences

The following table highlights the fundamental differences between a Section 8 company and an NBFC-MFI for micro finance operations:

| Parameter | Section 8 Company | NBFC-MFI |

|---|---|---|

| Governing Law | Companies Act, 2013 (Section 8) | RBI Act, 1934 + Companies Act, 2013 |

| Regulator | MCA / ROC | Reserve Bank of India (RBI) |

| Micro Finance Allowed? | No (Prohibited by MCA Circular 05/2022) | Yes (With valid CoR from RBI) |

| Minimum NOF | No statutory minimum | ₹10 crore |

| Profit Distribution | No dividend — profits reinvested in objects | Profit distribution is allowed as per the company law |

| Lending Capacity | Severely limited — cannot operate as a lending business | Full microfinance lending authorised |

| RBI Supervision | Not directly supervised | Subject to RBI inspection, reporting, and prudential norms |

| Capital Adequacy | Not applicable | 15% CRAR required |

| Qualifying Assets | Not applicable | 60% of total assets must be microfinance loans |

| Scale of Operations | Very limited | Can scale nationally with adequate capital |

What About Existing Section 8 Companies Already Doing Micro Finance?: The RBI Master Direction on Regulatory Framework for Microfinance Loans, 2022 (Paragraph 9) addresses the position of existing Section 8 (not-for-profit) companies engaged in microfinance activities. The key provisions are as follows:

- The exemption from Sections 45-IA, 45-IB, and 45-IC of the RBI Act, 1934, has been withdrawn for not-for-profit companies engaged in microfinance activities that have an asset size of ₹100 crore and above. Such companies are required to register as NBFC-MFIs with the RBI.

- Not-for-profit companies that are not eligible for exemption (i.e., those with assets of ₹100 crore and above) are required to submit an application for NBFC-MFI registration to the RBI within three months of the issuance of the circular. If they do not currently comply with NBFC-MFI regulations, they must submit a board-approved plan with a roadmap to meet the prescribed requirements.

- For smaller Section 8 companies (below ₹100 crore in assets) that were exempted earlier, the definition of microfinance loans has been aligned with the new framework — collateral-free loans to households with annual income up to ₹3 lakh.

In simple terms, the RBI is progressively bringing all microfinance activity under its regulatory oversight, and the era of unregulated microfinance through Section 8 companies is effectively over. 🔒

Penalties and Consequences of Violation: Operating a microfinance business without proper RBI authorisation carries serious consequences under the following provisions:

- Section 45-IA of the RBI Act, 1934 — Carrying on financial business without a Certificate of Registration is an offence. The RBI can issue directions for cessation of such activities.

- Section 8(9) of the Companies Act, 2013 — If a Section 8 company contravenes any of the conditions subject to which a licence was granted, the Central Government may revoke the licence and direct its winding up. The company, and every officer in default, shall be punishable with a fine of up to ₹25 lakh. The directors and managers may also face imprisonment for up to 3 years.

- ROC Action — As directed by MCA General Circular No. 05/2022, ROCs are actively monitoring Section 8 companies to ensure that none of them carries out micro finance activities. Any attempt to alter the object clause for this purpose will be rejected at the e-form processing stage itself.

Conclusion

To start a microfinance business in India, RBI approval is mandatory. Section 8 companies are not permitted to conduct microfinance activities, as clarified by MCA’s General Circular No. 05/2022. The RBI’s regulatory framework, including the Master Direction on Microfinance Loans, 2022 and the Scale-Based Regulation Framework, governs this sector. To proceed, one must form a company, secure the requisite ₹10 crore NOF, and apply for NBFC-MFI registration with the RBI. Contact SetIndiaBiz for end-to-end NBFC-MFI registration assistance.

Frequently Asked Questions (FAQs) 💬

Can I register a Section 8 company with microfinance as its main object?

Why did MCA ban Section 8 companies from doing microfinance?

What is the minimum capital required to start a microfinance business legally?

Can an existing Section 8 company convert itself into an NBFC-MFI?

Is the RBI exemption for Section 8 micro finance companies still valid?

What kind of loans can an NBFC-MFI provide?

How long does the NBFC-MFI registration process take?

In This Article

Author Bio

Setindiabiz Editorial Team is a multidisciplinary collective of Chartered Accountants, Company Secretaries, and Advocates offering authoritative insights on India’s regulatory and business landscape. With decades of experience in compliance, taxation, and advisory, they empower entrepreneurs and enterprises to make informed decisions.