Introduction: Input Tax Credit (ITC) is the credit of GST that a registered person is entitled to claim, under Section 16 of the Central Goods and Services Tax Act, 2017, on tax paid on inward supplies of goods or services used or intended to be used in the course or furtherance of business, to be set off against the GST payable on outward supplies. This page sets out the meaning of the Input Tax Credit, the eligibility conditions under Section 16, the items on which credit is blocked under Section 17(5), and the time limit for availing ITC.

Input Tax Credit

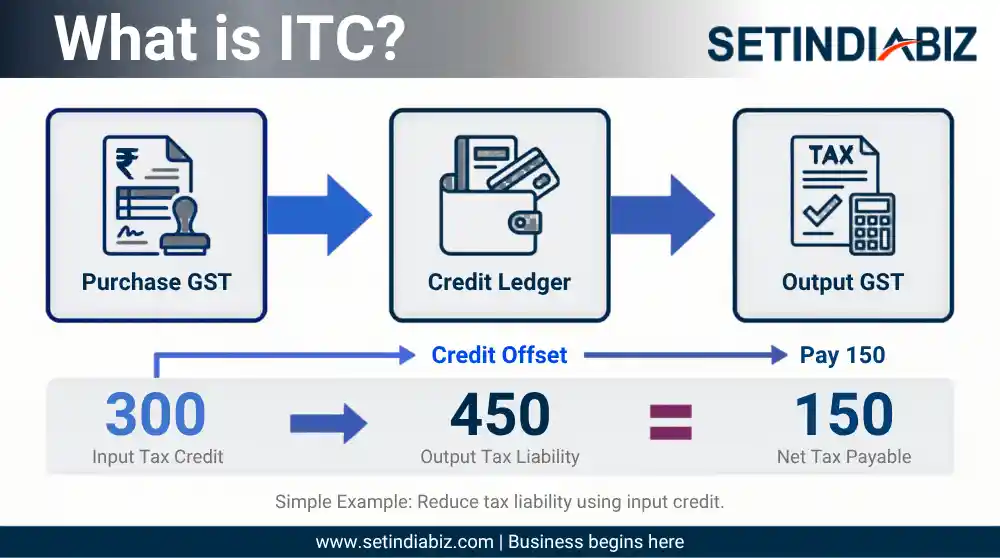

Input Tax Credit allows a GST-registered business to deduct the tax already paid on its purchases from the tax it collects on its sales, so that GST is borne only on the value the business itself adds. When a registered person buys taxable goods or services for business use, the GST charged by the supplier is credited to the buyer’s electronic credit ledger and can be used to discharge output GST liability under Section 49 of the CGST Act.

ITC is not an automatic right

The input Tax Credit under GST is conditional on the buyer holding a valid tax invoice, the supplier having furnished the invoice in GSTR-1 so that it appears in the buyer’s GSTR-2B, the buyer having received the goods or services, and the tax having actually been paid to the Government. Credit is permanently denied on a list of items under Section 17(5) (blocked credits), and is unavailable to taxpayers under the Composition Scheme under Section 10 of the CGST Act.

Eligibility Conditions for ITC U/s 16(2)

| No | Condition | Statutory Requirement |

|---|---|---|

| 1 | Possession of an invoice | Buyer must hold a valid tax invoice or debit note from a registered supplier. See Section 16(2)(a) |

| 2 | The invoice must reflect in GSTR-2B | Supplier must have furnished the invoice in GSTR-1, and the details must be communicated to the buyer — Section 16(2)(aa) |

| 3 | Credit not restricted | Credit communicated to the buyer must not be restricted under Section 38. See Section 16(2)(ba) |

| 4 | Receipt of goods or services | Buyer must have actually received the goods or services, including bill-to-ship-to deliveries. See Section 16(2)(b) |

| 5 | Tax paid to the Government | The supplier must have paid the tax charged on the supply to the Government. See Section 16(2)(c) read with Rule 37A |

| 6 | Return filed | Buyer must have furnished the return under Section 39. See Section 16(2)(d) |

| 7 | Payment to the supplier | Buyer must pay the supplier the amount due, plus tax, within 180 days of the invoice date; failure to do so triggers a reversal with interest. See second proviso to Section 16(2) read with Rule 37 |

| 8 | Time limit | Earlier than 30 November, following the financial year of the invoice, or the filing of the annual return. See Section 16(4) |

Legal Provisions

For the operative statutory language, refer to Section 16 and Section 17(5) of the Central Goods and Services Tax Act, 2017. The Bare Act and Rules are available on the Central Board of Indirect Taxes and Customs website at cbic-gst.gov.in.

FAQ’s

What is the difference between input tax and Input Tax Credit?

Under which section of the CGST Act is Input Tax Credit governed?

What are the conditions to claim Input Tax Credit under Section 16?

In This Article

Author Bio

Meet Sanjeev Kumar, a distinguished advocate before the Supreme Court of India, High Courts, and National Tribunals. Founding Partner of Juriskps Law Offices, a premier law firm, he specializes in commercial, corporate, tax, arbitration, and IPR matters. His incisive legal insights enrich Setindiabiz’s blog with expert commentary.