GST LUT filing is a critical annual compliance task for every Indian exporter. As we enter FY 2026-27, businesses exporting goods or services must complete this task — filing the Letter of Undertaking (LUT) under GST. Valid for only one financial year, the LUT lets you export without paying IGST upfront. This guide covers the exact legal requirements, the step-by-step GST LUT filing process, and the financial consequences of not filing before your first export of FY 2026-27 — advisable by 31st March 2026 to ensure seamless operations from Day 1.

Table of Contents

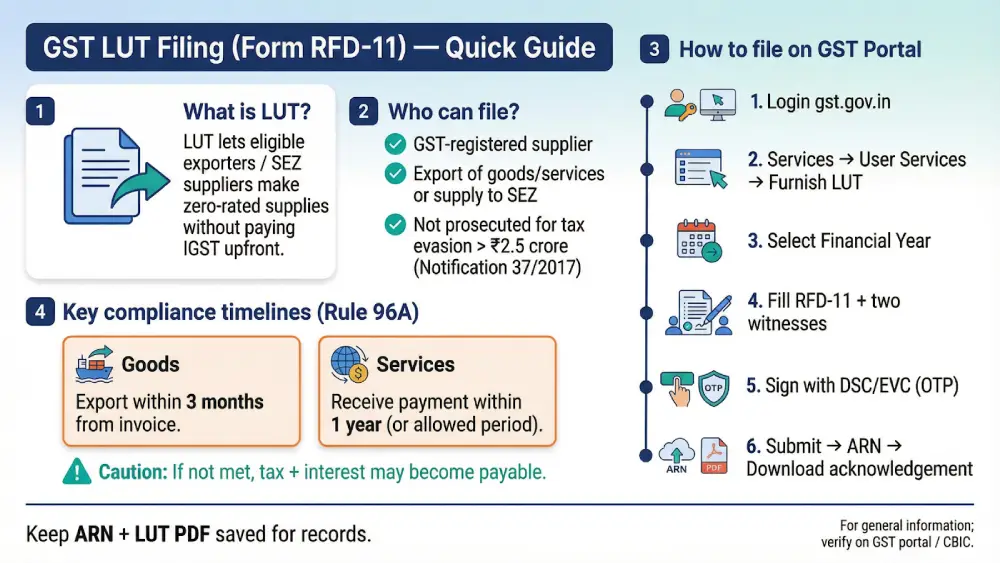

What is LUT Under GST?

Under Section 16 of the Integrated Goods and Services Tax (IGST) Act, 2017, exports and supplies to Special Economic Zones (SEZs) are classified as “zero-rated supplies.” This ensures that Indian exports are not burdened by domestic taxes, keeping businesses globally competitive.

By submitting a Letter of Undertaking (LUT) via Form GST RFD-11, an exporter formally declares to the tax authorities their commitment to export the specified goods or services within the stipulated period.

This legal promise allows the exporter to bypass the upfront payment of Integrated Goods and Services Tax (IGST).

Essentially, the LUT serves as an undertaking that the exporter will comply with all export compliance requirements and agrees to pay the applicable tax, along with interest, should the export commitment not be fulfilled.

Why is LUT Filing Critical for FY 2026-27?

As per Rule 96A of the Central Goods and Services Tax (CGST) Rules, 2017 (notified via GST Notification No. 16/2017 dated 07-07-2017), any registered taxpayer wishing to export without paying integrated tax must furnish this declaration before the actual export takes place.

Without valid GST LUT filing completed prior to your first export or SEZ supply of FY 2026-27 (practically, before 31st March 2026 to avoid Day-1 disruption), your exports will not be treated as tax-exempt by default.

You will be required to pay the full IGST amount upfront during export clearance and then go through the time-consuming process of claiming a refund under Section 54 of the CGST Act, 2017 via Form GST RFD-01.

The core benefit of GST LUT filing is preserving your working capital. IGST refunds typically take weeks to months, depending on the accuracy of the documentation and departmental processing. An active LUT keeps your cash liquid and available for core business operations.

| Parameter | With LUT (Form RFD-11) | Without LUT (IGST + Refund Route) |

|---|---|---|

| Upfront Tax Payment | ❌ Not required | ✅ Required |

| Working Capital Impact | None | Funds blocked until refund |

| Refund Process | Not applicable | RFD-01 filing required |

| Processing Time | Instant ARN on submission | 2–6 months typically |

| Paperwork | Minimal | Extensive documentation |

| Recommended For | Regular exporters | Occasional/one-off exports |

Who Must File Form GST RFD-11?

The GST LUT filing requirement applies to all GST-registered taxpayers engaged in zero-rated supplies with a clean compliance record. This includes:

- Exporters shipping physical goods outside India

- Businesses supplying goods or services to SEZ units or SEZ developers within India

- Service providers exporting services to overseas clients (e.g., IT, consulting, design firms, freelancers, independent consultants and service providers)

| The only legal restriction: If a taxpayer has been prosecuted for tax evasion exceeding ₹2.5 Crore under the CGST Act or the IGST Act, they are barred from using the LUT facility. Such entities must instead furnish an Export Bond with a bank guarantee — a significantly more capital-intensive process. |

Note: Exporters of goods must register under GST regardless of turnover under Section 24(i) of the CGST Act, 2017, since exports are zero-rated (not exempt) inter-state supplies.

However, service exporters with aggregate turnover below ₹20 lakh may be exempt from mandatory registration under Notification No. 10/2017-Integrated Tax dated 13.10.2017.”

How to File GST LUT Online (Step-by-Step)

The government has fully digitised the LUT filing process. Here is how to do it:

Step 1: Log in to the GST Portal. Visit gst.gov.in and log in with your valid GSTIN credentials.

Step 2: Navigate to the LUT Section. Go to Services → User Services → Furnish Letter of Undertaking (LUT). Form GST RFD-11 will open with your basic business details pre-filled.

Step 3: Select Financial Year. For your GST LUT filing, choose “2026-27” from the ‘LUT Applied for Financial Year’ dropdown.

Step 4: Fill in Required Details. Provide the names, occupations, and addresses of two independent witnesses as required by the legal declaration.

Step 5: Self-Declaration Tick all three mandatory self-declaration checkboxes, confirming that you will:

- Export goods/services within the prescribed timeline (3 months for goods),

- 1 year for foreign exchange realisation on services

- Comply with all provisions of the CGST Act, IGST Act, and allied rules

- Pay IGST with interest under Section 50(1) of the CGST Act, 2017 (generally 18% p.a. as notified) from the invoice date if the export obligation is not fulfilled

Step 6: Sign and Submit

- Companies and LLPs: Must use a Digital Signature Certificate (DSC)

- Proprietorships and Partnerships: Can verify using an Electronic Verification Code (EVC) via OTP

Step 7 — Download Acknowledgement Upon successful GST LUT filing submission, the system generates an Application Reference Number (ARN). Download the acknowledgement slip immediately.

⚠️ Application Statuses to Know: After filing, your LUT can show statuses like Submitted, Pending for Clarification, Approved, Deemed Approved (if the tax officer takes no action within 3 working days), or Rejected. The LUT status changes to Expired automatically at the end of FY 2026-27.

Consequences of Not Filing LUT

Immediate Impact: Without active GST LUT filing, customs authorities and the GST network will treat your export as a standard taxable supply.

You will be required to pay full IGST upfront before goods are cleared — severely disrupting cash flow and potentially delaying delivery timelines and damaging buyer relationships.

Post-Filing Rules Under 96A(1)

| Condition | Goods Export | Services (Foreign Exchange) |

|---|---|---|

| Time Limit to Comply | 3 months from invoice date | 1 year from invoice date |

| Payment Trigger on Default | IGST + interest payable within 15 days of expiry of the 3-month window | IGST + interest payable within 15 days of expiry of the 1-year window |

| Consequence of Default | LUT facility withdrawn | LUT facility withdrawn |

| Interest Rate | As per Section 50(1) CGST Act (generally 18% p.a. as notified) from the invoice date | As per Section 50(1) CGST Act (generally 18% p.a. as notified) from invoice date |

Filing your GST LUT filing retroactively does not help. IGST liability accrues for every export invoice raised before the LUT was on record. There is no late-filing grace provision under Rule 96A.

Conclusion

GST LUT filing (Letter of Undertaking) is a straightforward but mission-critical compliance step that directly determines the financial health of your export business.

By filing Form GST RFD-11 before your first export of FY 2026-27, ideally by 31st March 2026, you protect your working capital, avoid IGST refund delays, and remain fully compliant with Indian tax law.

Don’t wait until the last day — log in to the GST portal today and lock in your zero-rated supply benefits for all of FY 2026-27.

FAQ’s

What happens if I export goods without filing the LUT for FY 2026-27?

Can a previously filed LUT be automatically renewed for the new financial year?

Is there a penalty if I fail to export goods after filing an LUT?

Do I need to submit physical documents after filing the LUT online?

What is the filing fee for an LUT?

Can I file the LUT after April 1 if I missed the deadline?

This guide covers the exact legal requirements, the step-by-step filing process, and the financial consequences of not filing before your first export of FY 2026-27 — advisable by 31st March 2026 to ensure seamless operations from Day 1.

In This Article

Author Bio

Setindiabiz Editorial Team is a multidisciplinary collective of Chartered Accountants, Company Secretaries, and Advocates offering authoritative insights on India’s regulatory and business landscape. With decades of experience in compliance, taxation, and advisory, they empower entrepreneurs and enterprises to make informed decisions.