Overview: Statutory Audit under the Companies Act 2013 is one of the major requirements for Private Limited Companies incorporated in India. This blog explains some of its crucial aspects, like legal framework, prescribed deadlines, eligibility criteria, the appointment of an auditor, benefits, and consequences of not conducting timely audits. A thorough reading of the blog will impart full information about this crucial compliance and ensure your company’s adherence to regulatory standards. For further guidance, you are free to contact our startup advisors!

A company’s audit serves as an indispensable mechanism for examining its activities, compliance, and financial records. There are several types of audits that can be conducted for a variety of purposes. For instance, we have the tax audit to verify the taxable income and claimed deductions; a cost audit to examine the costs and expenses in business operations; and, most importantly, a statutory audit to comply with the requirements of the Companies Act. While tax audits and cost audits are conducted by professionals, statutory audits under the Companies Act 2013 are conducted by an auditor appointed by the company itself. Let’s dig deeper into the related processes and requirements.

Legal Framework for Statutory Audit under Companies Act 2013

Statutory Audit under the Companies Act 2013 is mandatory for all types of companies in India. Section 139 of the Act prescribes an auditor’s appointment for this purpose. According to this section, every company is required to appoint an auditor at its first annual general meeting (AGM), who shall hold office from the conclusion of that meeting till the conclusion of the sixth AGM. However, the entire term is subject to ratification in every AGM conducted during subsequent years.

Additionally, subsection (2) of Section 139 specifies the eligibility criteria for auditors. An individual or a firm, including a limited liability partnership (LLP), can be appointed as an auditor, provided they are qualified and eligible. We have discussed the eligibility criteria further in this blog. Section 143 of the Companies Act delineates the powers and duties of the appointed auditors. This includes the auditor’s responsibility to prepare a detailed report on the financial status of the company.

Such a report requires an in-depth examination of the company’s financial statements, which include the balance sheet, profit and loss account, and cash flow statement. The audit report must state whether the financial statements give a true and fair view of the company’s state of affairs. Lastly, the Companies Act emphasises the need for compliance with auditing standards, as mentioned in Section 143(10). This section requires auditors to follow the auditing standards notified by the Central Government.

Is Statutory Audit Mandatory for All Companies?

Statutory audit under the Companies Act 2013 is compulsory for every company, irrespective of its turnover. Even if a company is smaller in size and falls within the definition of a one-person or small company, it is still required to undergo a statutory audit. The Act mandates this process to ensure a comprehensive examination of the company’s financial statements, contributing to financial transparency, credibility, and accountability across the corporate landscape. The statutory audit requirement underscores the significance of accurate and reliable financial reporting, reinforcing the regulatory framework’s commitment to upholding corporate governance standards for businesses of all sizes.

Due Date for Conducting Statutory Audit under Companies Act 2013

Statutory audit under the Companies Act 2013 is conducted annually and should be completed within six months from the end of the financial year. This means that if a company’s financial year concludes on March 31st, the statutory audit must be finished by September 30th of the same year. Wondering Why? Let’s understand! Meeting the statutory audit deadline is intricately connected to other crucial timelines within the regulatory framework.

Firstly, the completion of the audit is pivotal for the timely convening of the Annual General Meeting (AGM). As per the Companies Act, the AGM should be held within six months of the end of the financial year. Therefore, concluding the statutory audit by the specified deadline ensures that the AGM can be convened promptly, allowing shareholders to review and approve the audited financial statements.

Additionally, the due date for the statutory audit aligns with the deadline for filing the audited financial statements to the Registrar of Companies (ROC) through the AOC-4 form. The AOC-4 form is required to be filed within 30 days of the conclusion of the AGM. Meeting the statutory audit deadline becomes pivotal in this context, ensuring that the audited financial statements are ready for submission, promoting regulatory compliance, and avoiding penalties associated with delayed filing.

Appointment of Auditor for Conducting Statutory Audit

Ensuring a methodical and complaint procedure for the appointment of an auditor is pivotal for a successful statutory audit under the Companies Act 2013. The procedure encompasses the initial appointment of the first auditor, followed by appointments of subsequent auditors at the end of every year. It’s completed when an intimation is filed with the ROC in form ADT-1. Let’s briefly understand what the process of appointment is.

First Auditor Appointment under the Companies Act

Ensuring a meticulous and compliant process for the appointment of the first auditor is imperative within the initial 30 days of incorporation. The Board of Directors convene a meeting to pass a resolution for the purpose. As a result, either an individual or a CA firm qualified to become an auditor gets appointed. In the event the Board fails to appoint the first auditors within the stipulated 30 days, shareholders can step in by appointing auditors through an extraordinary general meeting within 90 days, in accordance with Section 139(6).

Before the appointment, the chosen auditor provides formal consent, signifying their willingness to undertake the responsibilities. This is in addition to declaring their eligibility for the appointment itself. The first auditor holds office until the first Annual General Meeting’s conclusion. At the second AGM, shareholders have the opportunity to ratify the appointment, deciding whether to retain the auditor for subsequent years or not.

Subsequent Auditor Appointment

Following the first auditor appointment, a systematic process unfolds for the subsequent auditor appointments. During the first AGM of the company post-incorporation, shareholders pass a resolution to appoint subsequent auditors for a five-year term, adhering to the guidelines mentioned in Section 139(1) of the Companies Act. As this term concludes, a fresh auditor is appointed in subsequent AGMs to ensure compliance with the regulatory standards. This structured approach to auditor appointments not only contributes to efficient corporate governance but also emphasises transparency and accountability in financial reporting.

Note: The details of the auditor’s appointment, be it initial or subsequent, must be communicated to the ROC within 15 days of the AGM or Board meeting where the appointment occurs. This shall be done in adherence to Sections 139(1) and 139(8) of the Companies Act.

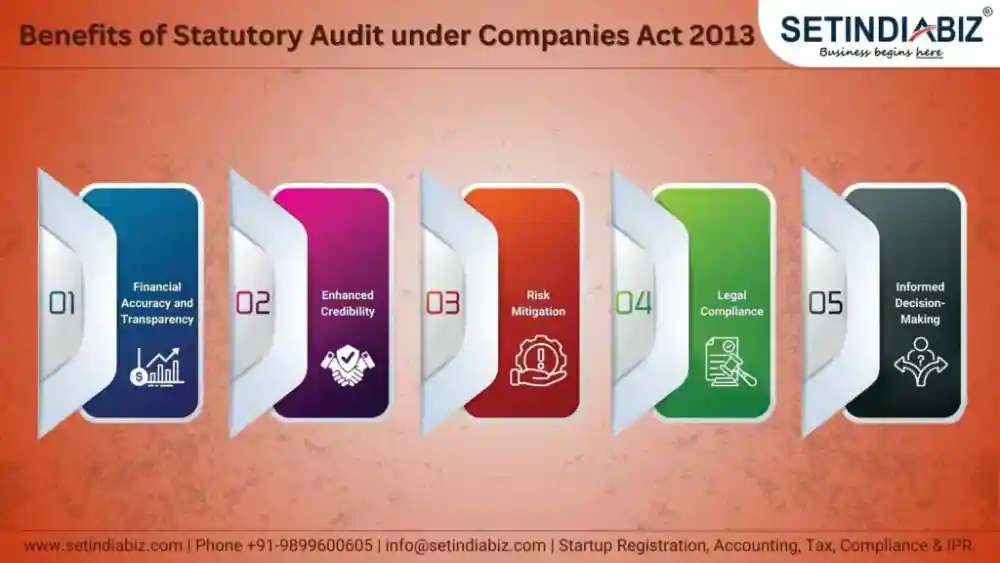

Benefits of Statutory Audit under the Companies Act 2013

Conducting a statutory audit under the Companies Act 2013 provides multifaceted advantages to companies that transcend mere regulatory compliance. Beyond meeting legal requirements, statutory audits offer invaluable insights, foster financial credibility, and fortify corporate governance. The benefits extend to all stakeholders, management, and the company’s overall operational efficiency. A few prominent benefits are listed below:

- Financial Accuracy and Transparency: Statutory audits meticulously examine financial statements, ensuring accuracy and transparency. This not only complies with regulatory standards but also instils confidence in stakeholders regarding the company’s financial health.

- Enhanced Credibility: The audited financial statements lend an enhanced level of credibility to the company’s financial reporting. Investors, creditors, and other stakeholders rely on audited accounts for informed decision-making, bolstering the company’s reputation in the market.

- Risk Mitigation: Through in-depth scrutiny, statutory audits identify and mitigate financial risks. This proactive risk management contributes to the prevention of financial irregularities and fraud, safeguarding the company’s assets and interests.

- Legal Compliance: Compliance with statutory audit requirements ensures adherence to legal standards, shielding the company from potential legal issues. It demonstrates a commitment to corporate governance and regulatory responsibility.

- Informed Decision-Making: Management gains valuable insights from the audit process, enabling informed decision-making. The audit highlights areas for improvement, financial efficiency, and potential growth strategies, empowering management to steer the company strategically.

Legal Consequences of Not Conducting a Statutory Audit

Failure to conduct a statutory audit under the Companies Act 2013 carries significant legal consequences. This includes specific fines and penalties imposed on various stakeholders. These legal consequences underscore the significance of statutory audits in the regulatory landscape, emphasising the financial implications for companies and auditors who neglect this fundamental requirement. Businesses must prioritise compliance to avoid such legal penalties and safeguard their financial and legal standing. Check out the details of fines and penalties imposed below:

- Fines for Companies: Section 147 of the Companies Act stipulates that a company failing to conduct a statutory audit may face fines ranging from INR 25,000 to INR 5 lakhs.

- Fines for Auditors: Auditors themselves are subject to penalties under Section 147. If an auditor fails to comply with audit obligations, they may face fines ranging from INR 25,000 to INR 5 lakhs.

- Continued Non-Compliance: In cases of persistent non-compliance, the Companies Act allows for daily fines until compliance is met. The daily penalty can range from INR 500 to INR 5,000 for both companies and auditors.

Other Types of Audit under Companies Act, 2013

Beyond the statutory audit, the Companies Act 2013 encompasses various other audit mechanisms designed to ensure comprehensive oversight and regulatory compliance. These audits serve distinct purposes, addressing specific aspects of a company’s operations and financial reporting. Understanding and incorporating these diverse audit mechanisms into a company’s governance framework goes beyond statutory requirements, contributing to a robust and well-rounded approach to financial management, compliance, and risk mitigation. Each type of audit plays a unique role in ensuring the overall health and integrity of a company’s operations.

- Internal Audit: Conducted internally by the company’s team or outsourced professionals. Focuses on evaluating and improving the effectiveness of internal controls and risk management.

- Cost Audit: Mandated for certain specified companies. Examines the cost records to ensure adherence to cost accounting standards.

- Secretarial Audit: A comprehensive review of the company’s compliance with legal and regulatory requirements. Conducted by a qualified company secretary to ensure adherence to statutory provisions.

- Tax Audit: Required under the Income Tax Act for companies meeting specified turnover criteria. Ensures accuracy and compliance with tax laws in financial reporting.

- Compliance Audit: Focuses on ensuring adherence to specific laws, regulations, and company policies. Aims to identify and rectify any instances of non-compliance.

- Operational Audit: Evaluates the efficiency and effectiveness of operational processes. Aims to enhance overall operational performance and identify areas for improvement.

Conclusion

The process of Statutory Audit under the Companies Act 2013 stands as a cornerstone for transparent financial reporting, regulatory compliance, and corporate governance. Aside from legal obligation, it serves as a robust mechanism for businesses to enhance credibility, mitigate risks, and provide stakeholders with accurate financial insights. Embracing the broader spectrum of audits outlined by the Companies Act ensures a holistic approach to financial management and regulatory adherence, promoting the long-term sustainability and resilience of businesses in today’s dynamic corporate landscape.

FAQ’s

What is a Statutory Audit under Companies Act 2013?

Who is eligible to conduct a Statutory Audit under Companies Act 2013?

What are the legal consequences of not conducting a Statutory Audit?

Are there other types of audits mandated under the Companies Act 2013?

Why is timely compliance for Statutory Audit crucial?

What documents must be submitted to the auditor for a statutory audit?

- Financial Statements

- Bank Statements & Ledgers

- Tax Returns

- Minutes of Board/AGM Meetings

- Loan Agreements

Are startups exempted from statutory audits?

Can a disqualified director appoint a statutory auditor?

Can an LLP be appointed as a statutory auditor?

What if statutory audit deadlines are missed?

- Company: fines of ₹25,000–₹5 lakhs + ₹500–₹5,000/day for continued default.

- Auditor: he/she may face disqualification for 5 years if the cause of non-compliance is deliberate.

In This Article

Author Bio

Setindiabiz Editorial Team is a multidisciplinary collective of Chartered Accountants, Company Secretaries, and Advocates offering authoritative insights on India’s regulatory and business landscape. With decades of experience in compliance, taxation, and advisory, they empower entrepreneurs and enterprises to make informed decisions.